Clarke CEO George Armoyan at the 2014 Sherritt annual meeting. Photo: Andrew Francis Wallace/Toronto Star

As the prices for nickel and oil plunged in 2015, so did Sherritt International’s prospects of emerging on the other side of the commodity oversupply abyss. Sherritt’s main businesses are nickel and oil production in Cuba; nickel accounts for 72% of revenue.

In 2015, nickel was down 40% and the price for a barrel of oil fell 50%. Last week, Sherritt (S-T) reported Q4 and full-year earnings that reflected the dire situation. Revenue dropped 10% in 2015, adjusted EBITDA fell 55% and the net loss from continuing operations skyrocketed 559%, to $7.05 per share.

This is the story of how an anti-establishment value investor launched a proxy fight against Sherritt International that he lost, booking a $17.5-million gain in the process.

Sherritt’s latest venture is the Ambatovy laterite nickel mine, where it is a 40% partner and operator. The company took a $1.6-billion impairment on the Madagascar mine, which resulted in a breach of the financial debt-to-equity covenant in Sherritt’s credit facilities. Partners Sumitomo and Korea Resources Corp. (KORES) have responded to cash calls by providing further funding, which has not been matched by Sherritt. Negotiations with creditors continue.

Sherritt’s stock has been pummelled, steadily sliding from levels approaching $10 in early 2011 to the current 0.64 -- with the exception of a brief surge in the spring of 2014 that saw the stock rise from below $3 to the high $4s. It was a rare period of rising nickel prices.

In December of 2013, Sherritt had sold its thermal coal portfolio in Alberta and Saskatchewan to Westmoreland Coal for $465 million and its coal and potash royalty portfolio to Altius Minerals for $481 million.

Sherritt’s exit from the coal business was fortuitous, in hindsight. But Sherritt CEO David Pathe’s statements that he intended to put the proceeds to work purchasing another asset raised the ire of dissident shareholder George Armoyan, the activist investor who runs Halifax-based Clarke Inc (CKI-T).

Armoyan’s Clarke, a publicly traded investment firm, had quietly acquired a 5% plus stake in Sherritt, giving it the power to requisition a special meeting of shareholders. Clarke’s MO is to buy into undervalued or under-performing companies, extract value by restructuring or shifting focus, then exiting the position. One recent example was Clarke’s sale of its freight transportation business to Transforce in January 2014 for $100.5 million.

Armoyan, a Syrian immigrant, fired his opening salvo after Sherritt’s coal sale was announced.

Armoyan ramped up his campaign in the first months of 2014, blasting Sherritt on several fronts, including:

- the plan to buy more assets instead of paying down debt;

- executive compensation (Sherritt CEO David Pathe made $2.77 million in 2012 and directors collectively made $3.7 million);

- lack of insider equity ownership (directors and management owned less than .25% of oustanding shares).

Armoyan proposed three directors for the Sherritt board -- one of them, himself -- and unveiled several corporate governance initiatives, including shareholder “say on pay” for executive compensation. One of the director nominees was Armoyan himself and another was Ashwath Mehra, who ran Glencore’s nickel and cobalt businesses for 10 years.

Sherritt chairman Harold “Hap” Stephen, a veteran corporate executive, responded by blasting Armoyan’s bid in a letter to shareholders. Stephen said Armoyan lacked mining and international business experience and said his campaign threatened “to throw a wrench” into Sherritt’s progress, at a time when the company was “gaining momentum with a disciplined strategy to pay down debt, cut costs and focus on our core area of expertise.”

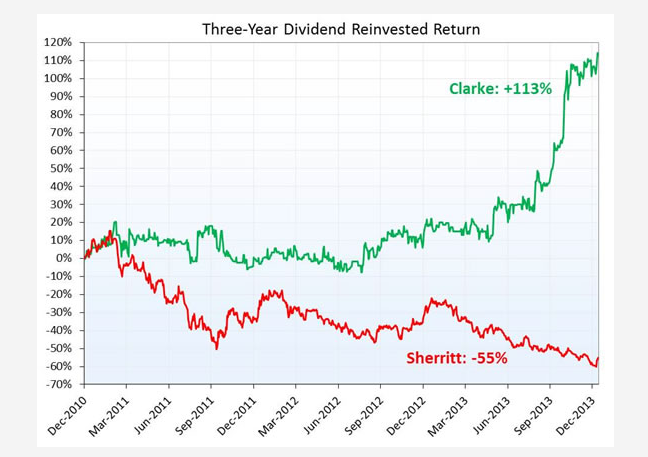

Ammunition for Clarke's 2014 proxy fight against Sherritt International

Fast-forward to the shareholder meeting. Sherritt won the proxy battle: its director nominees were handily elected and Armoyan suffered a rare defeat. He won a round of applause at the shareholder meeting, however, for saying that the company had good potential and was making progress toward enhancing shareholder value.

Sherritt moved on some of his demands, including special allowances for directors (they were being compensated for the Helms-Burton travel ban to the United States) and a focus on debt reduction instead of acquisitions. Armoyan said he would remain a shareholder, telling the Financial Post's Peter Koven: “I’m not the smartest guy in the world. (But) I’m the most persistent son of a bitch you’ll ever meet.”

A detail in Clarke’s second-quarter financials, filed a few months later, did reveal a few smarts, however. Clarke announced it had sold off all its Sherritt shares while there were tailwinds on the stock, booking a $17.5-million gain in the process.

Clarke's latest target is Northern Frontier (FFF-V), an oilpatch services and infrastructure firm. That investment hasn't worked out quite so well -- Northern Frontier shares are down 45% in the past year. Clarke funds own more than 14% of outstanding shares.

As for Sherritt, directors and executives have largely avoided the shareholder value destruction that has occurred -- their holdings still add up to less than .2% of outstanding shares. Directors and executives at Sherritt made $7.8 million in 2014, down from $8.5 million in 2013, according to page 140 of Sherritt’s 2014 annual report.

Sherritt International (S-T)

Price: 0.64

Shares outstanding: 294 million

Market cap: $188 million

1-year return: -69%

5-year return: -93%

Nickel - US$3.72/lb

1-year return: -42%

5-year return: -71%

Clarke Inc. (CKI-T)

Price: $9.10

Shares outstanding: 15.6 million

Market cap: $142 million

1-year return: -9%

5-year return: 109%

Join the conversation and tap into sharp analysis and commentary at CEO Terminal, the investment conference in your pocket.