The “make fast cash flipping houses” ads are back in force, construction is resurgent, consumers are walking around with shopping bags again, “mom & pop investors” are raising their 401k contributions, and US equities have healed their financial crisis wounds, rising to all-time highs. Animal spirits are also on the rise. You can see it. You can feel it in your bones. People are starting to feel confident, rappers aren't rapping about the “down economy” anymore, and the mainstream media has finally caught onto the fact that the stock market isn’t going to zero. Instead, it looks like it's going to infinity.

I have a sneaking suspicion that equities and high-yield credit are approaching bubble territory, but the market gods are the ultimate arbiters on that. What I am confident about is that we’re in the midst of a bubble in the “cash is trash” investor mindset.

I have a sneaking suspicion that equities and high-yield credit are approaching bubble territory, but the market gods are the ultimate arbiters on that. What I am confident about is that we’re in the midst of a bubble in the “cash is trash” investor mindset.

According to the transitory bubble theory, we know that at any given moment, there's going to be a bubble brewing somewhere. And with each bubble, a set of conventional wisdom and “market mantras” evolve. For example, during the 2005-2007 credit bubble, we were subjected to tropes like:

“The world is awash in liquidity.”

“Subprime is contained.”

“Soft landing in US housing.”

“The BRICs have decoupled from the US.”

We later learned these mantras -- and the conventional wisdom of this market period -- were unanimously wrong.

Consider also the 2008-2009 financial crisis, when analysts began using expressions like:

“Cash is king."

“Bathtub bottom.”

“Stock up on canned food, silver bars, bottled water, guns, and ammo.”

“Commercial real estate won’t come back for at least a decade.”

“An entire generation of investors has permanently left the stock market.”

And today, with the Dow, S&P 500, and Russell 2000 all at nominal all-time highs, the cliches circulating are:

“Cash is trash.”

“Equities are the only game in town.”

“Cash in a savings account is useless.”

“The Fed has your back” OR “The Fed is underneath you.”

“Central banks have removed tail risk from markets.”

I could go on, but you get the point: the “cash is trash” mantra's essentially taking investor psychology by force. The Fed has perhaps been the primary player perpetuating this disrespect, pretty much scoffing at any mention of holding significant cash. And rising equity prices and a solid upturn in housing prices have fanned the flames. Why make 1% in a savings account, when you can easily make 10-15% by investing in a home or raising your 401k contribution? This investor psychology is made even more attractive by the pervasive idea that "the Fed has your back,” and wants you to make money by investing in equities and real estate.

There's definitely truth to the above logic. But bubbles begin when a sound fundamental premise is taken to wild extremes by throngs of over-exuberant investors. In February 2009, for example, the conventional wisdom that “cash was king” turned out to be EXACTLY WRONG -- the vast majority of investors were figuratively cowering in their bunkers, clinging to soup cans and stacks of hundred dollar bills that they would have been better off investing in highly depressed equities and residential real estate.

And so it's my view that investors today are just as poorly positioned as they were in early 2009. The only difference is that instead of cash being king, cash is now trash. The pendulum has swung 180°, from extreme risk-aversion to extreme risk-taking. Cash offers optionality and flexibility where being fully invested makes you vulnerable to the whims of the market. Rising markets tend to convince short-sighted investors that the preceding period’s gains will continue indefinitely. And the fear of missing out in an environment of rising asset prices leads investors to “chase” investment opportunities and make irrational decisions. It's no different now.

As we enter the second quarter of 2013, virtually all risky assets are riding high. Even bitcoins (a digital pseudo-currency) bask in the glow of “cash is trash” fervor. However, as astute students of market history, we know that the times we need to be most vigilant are the times when everything seems so easy, when everyone's drinking the Kool-Aid. Currently, I prefer raising cash exposure and reducing equity and high-yield debt exposure as much as possible. Increasing one’s cash position will significantly lower overall portfolio beta at a time when the vast majority are amping their beta up. Cash also allows flexibility to take advantage of opportunities as they arise.

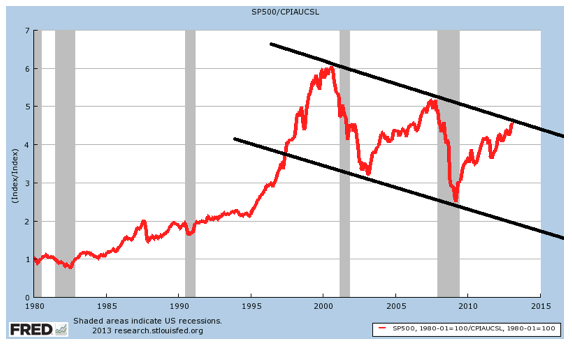

Here's a chart that should make astute market participants think twice about adding long-equity exposure right now:

S&P 500 adjusted for inflation

Fed Policy & Positioning Recommendations

At a time when most equity investors believe they can’t lose, I find it difficult to see how they can win, except in the very near term, or in specific situations. The early warning signs of inflation are becoming evident: real estate prices are picking up, landlords are raising rents for the first time in over five years, there's been no slack in rising food prices, and people are spending money, which inevitably drives up the price of goods and services.

There has never been a situation in history in which extraordinarily accommodative central bank monetary policy combined with surging asset prices did not lead to higher (oftentimes much higher) levels of inflation. In fact, we're seeing it happen in China right now. China experienced a stock market bubble that popped in late-2007. Its government responded with massive stimulus and highly accommodative polices, which caused the stock market bubble to transition into an epic property bubble. China has now found itself combating the simultaneous combination of high consumer price inflation, a property bubble, a decelerating economy, and highly uneven wealth distribution.

Many market observers have been perplexed at the Fed’s ability to drastically expand its balance sheet without having hardly any observable uptick in consumer price inflation. Of course, this is a complex subject and the relatively tame inflation levels have a lot to do with the massive pernicious deleveraging which was triggered as a result of the global financial crisis. However, I would argue that QE and other forms of government sponsored fiscal and monetary stimulus have largely benefited the wealthy while leaving the middle class and poor in roughly the same position they were in before the crisis.

QE and other programs such as the Treasury’s TALF benefit the wealthy holders of investment securities while punishing small time savers and low income earners with future inflation and currency debasement. Meanwhile, the wealthy tend to have little impact upon most of the items measured by the CPI, whereas, they have a hugely inordinate impact upon the prices of luxury and super-luxury items such as fine art, Lamborghinis, and high end yachts which have all seen significant increases in both demand and prices.

The below charts are a few years old but, make no mistake, the gap between the ‘haves’ and the many ‘have-nots’ has only widened further over the past few years:

Click to enlarge

By any estimation, the Fed ‘unwind’ will either be extremely difficult or flat-out impossible.Even if inflation should tick up to uncomfortably high levels, the Fed is most likely to respond by simply pausing its accommodative policy efforts and allowing its balance sheet to shrink by refraining from replacing maturing securities. Of course, even a gradual backing away from policy accommodation by the Fed will present huge headwinds for both the economy and markets – investors are likely to wonder what's next and be dissatisfied with any answers they might be able to come up with.

By any estimation, the Fed ‘unwind’ will either be extremely difficult or flat-out impossible.Even if inflation should tick up to uncomfortably high levels, the Fed is most likely to respond by simply pausing its accommodative policy efforts and allowing its balance sheet to shrink by refraining from replacing maturing securities. Of course, even a gradual backing away from policy accommodation by the Fed will present huge headwinds for both the economy and markets – investors are likely to wonder what's next and be dissatisfied with any answers they might be able to come up with.

Rising inflation expectations are also likely to lead to higher long-term bond yields, which will mean higher real interest rates. Higher rates and a steepening real rate term structure will by definition lead to falling asset prices as investors raise the discount rate with which they value future cash flows.

Of course, it’s possible the Fed will expand its balance sheet another few trillion dollars while asset prices surge even higher and inflation remains subdued. But the chances of this happening are pretty low. What was that Keynes quote about market remaining irrational?

Investors may be on the verge of realizing that just when they're thinking they can’t lose, they really need to look just over the horizon to see that almost the exact opposite is true. While equities and other risky assets such as high-yield corporate bonds and leveraged loans may continue to percolate just a bit longer, any additional gains are likely to be fleeting once investors’ begin to appreciate the enormity of their misperception. I really like the optionality and relative safety of US dollar cash. I also recommend relative value pairs trades such as:

- Long SPY/Short IWM

- Long DIA/Short IWO

- Long investment grade bonds/short high-yield bonds

- Long gold/short silver (or industrial metals such as copper, etc.)

- Selling upside call premium and using proceeds to add long put exposure on the major equity indices

CEO Technician, removing the fundamentals from the equation and focusing just on price, what would you do if the S&P index breakthroughs the the resistance line?