Oceanic's Trade Map (Company)

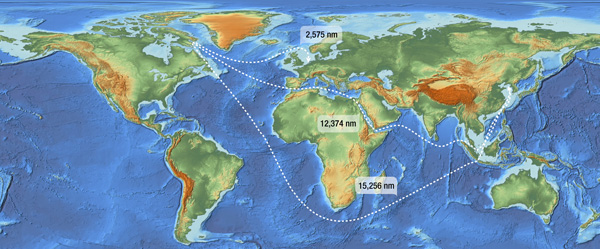

Oceanic Iron Ore (FEO:TSXV), the small cap iron ore developer, has received the results of a shipping optimization study to determine whether the benefit justifies the costs of year round shipping from the Company’s Hopes Advance project located in the Canadian Arctic. The study includes direct shipping during summer months and transshipment during winter months. The Company got input from Fednav Limited which has been shipping concentrates in the Canadian Arctic for over 15 years including Vale’s Voisey’s Bay mine and Glencore Xstrata’s Raglan mine. The transshipment locations identified in the study are Nuuk - Greenland, Rotterdam – Netherland and St Pierre and Miquelon.The cost of this type of shipping is anticipated to be approximately $31-$33 per tonne which will bring the project’s cash cost CFR China at $65 per tonne. Given the current spot price for CFR (62% iron) product is approximately $135 per tonne, the Hope’s Advance project remains a high margin project.

Alan Gorman, President/COO said: "We are pleased with the results of this independent Shipping Optimization Study led by AMEC. Further defining the shipping considerations associated with the Hopes Advance project is a critical development in respect of the Company's objective to secure a capable strategic partner. The involvement of Fednav, CSL, EMO, and others, adds the experience of these very reputable organizations and practical inputs that ensure product can be shipped at the lowest possible cost on a year round basis."

Oceanic’s News Release here: Oceanic Receives Results of Shipping Optimization Study

The ‘elephant in the room’ issue Oceanic faces is financing related. Although the company has a multi-billion dollar project (pre-tax NPV of $5.6 billion) and is advancing it through the necessary development stages, the reality is that the company has a market capitalization of $17 million and needs to raise $2.85 billion to build their mine. The pre-feasibility they put out in September of 2012 highlighted a situation whereby the project would be financed with 60% debt, assuming another 30% would come from a strategic Asian partner, the final 10% would still represent a $285 million equity raise (or even 5% would represent $142 million which would represent 8.35 times their current market capitalization). So, how do they finance the project without either; a, giving away the project or b, diluting the company to an unrecognizable point.

Today Alderon Iron Ore (ADV:TSX) signed an engagement letter with BNP Paribas to arrange a $1 billion debt facility for their Kami Project (which already has an Asian partner – Hebei Iron and Steel Group).

Here’s Alderon’s News Release: Alderon Announces Signing of Project Financing Engagement Letter

Oceanic Chairman and CEO, Steven Dean

Oceanic’s best alternative is to do what they are doing which is a feasibility study which should optimize costs and minimize capex. Also, the company needs to bring in a significant strategic partner to soak up, not only the initial capex, but also the development costs prior to construction start-up (which, by the way, I am sure they are well underway in talks with these groups). Given the team at Oceanic including Steven Dean who has a track record which includes being the President of Teck Cominco, Alan Gorman formerly with Goldbrook Ventures and a board that includes Gordon Keep and Gregg Sedun, the company has the right people in place to optimize the project to a point where it can create the most value for shareholders, whether that is selling the company or finding a creative financing solution.