When searching for opportunities in the junior sector, we like the focus to be on quantitative and empirical data. Sure, everyone likes a good anecdote about geologists kicking over rocks in the middle of nowhere, but the truth is nothing makes us happier than cold, hard numbers.

The most difficult aspect of a company to quantify is the management team. In a previous article, we highlighted one measure that we use called the General and Administrative Expense Ratio (G&A) which is one way of getting a glimpse as to how management puts shareholder money to work. In this article, we'll first look at why management and institutional ownership are important. Then, we’ll break down our data to show what the average numbers are like throughout the entire exploration lifecycle from green fields all the way to production.

'Skin in the Game'

Incentive options and warrants have their place, but when we are looking at management ownership, we are talking specifically about common shares. How much capital has the management team taken out of their pockets and put directly into the company? This vested interest, or 'skin in the game', shows how much the team believes in a project. Importantly, high ownership also is usually a sign that the company will respect shareholder dollars when making spending decisions. If management has no skin in the game, they don’t care if the share structure gets diluted or if the stock gets rolled back again. They can just re-issue incentive options when it looks like they can make a quick buck.

Using data from the 400+ precious metals companies we cover in Tickerscores, we took a look at the average common share ownership of companies. These average numbers are important benchmarks to consider when exploring buying opportunities in the market.

Quick note on the sample size: we used info on 413 companies based on Q2 financial data, and excluded majors from the analysis. These are mostly companies on the TSX and TSX-V.

Aside from the management team, another important ownership statistic we look at is institutional and fund ownership, which is what some would characterize as "the smart money".

'Smart Money'

In our analysis, we typically add both fund and institutional ownership together into one metric. This number represents the amount of shares of a company owned by funds or big financial institutions. Typically, this includes any ownership by banks, mutual funds, investment advisors, hedge funds, or similar firms. There are arguments towards both the pros and cons of fund ownership, but in the junior sector we mainly see it as a positive sign. The reason for this is that the junior sector is populated by many small and unproven companies. For a small junior to be backed by a sophisticated financial organization, it lends credibility.

If a respected group such as Sprott, Sentient Group, or KCR Fund (Katusa, Casey, and Rule) is buying shares of a company, this should be a signal to the retail crowd. It means that a sophisticated group has gone through extensive due diligence and is confident in the project and management team. These institutions and funds are big for a reason: they've made money in the past.

Here's the frequency chart for institutional and fund ownership. Note: an astounding 23% of companies have no such ownership at all.

For both management and institutional/fund ownership, the above distributions are very broad and encompass all types of companies in many different jurisdictions.

To narrow it down and make the data more interesting, we've broken it up based on the exploration lifecycle.

Not surprisingly, the average management ownership is highest when the shares are the cheapest (exploration) and the percentage is diluted as the company matures. Conversely, fund and institutional investment is at its lowest when the company is "riskiest" and increases as it gets closer to commercial production.

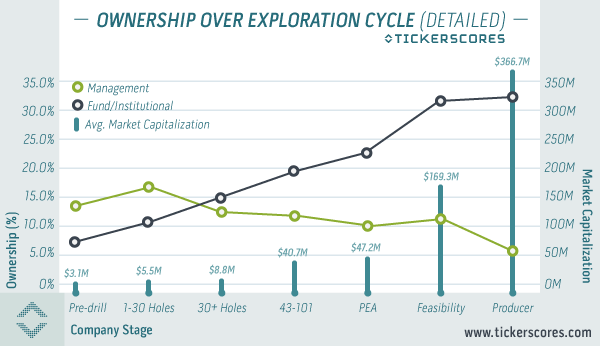

Let's drill down even further and break each stage into smaller stages. For exploration, we'll divide it into "Pre-drilling", "0-30 drill holes", and "30+ drill holes". For development, we'll break it into "NI 43-101 Technical Report", "Preliminary Economic Assessment (PEA)", and "Feasibility Study". For producers, we'll just group them as one category now.

Here are a few things worth noting. First, it looks like management ownership stays fairly constant through the development stage (11.2%, 10.1%, and 10.8% in Technical Report, PEA, and Feasibility sub-stages). This means as projects moves forward, on average, management is maintaining their interest. In contrast, the projects are now de-risked enough for funds and institutions to increase their ownership dramatically through those stages from 19.1% to 31.3%.

Another interesting point is that the rate at which institutional and fund ownership increases stays constant from pre-drilling all the way to the PEA. However, as soon as the Feasibility Study is completed, the "smart money" buys in at an increased rate. It jumps by over 8% between these two stages.

There can be big differences within each stage. In this case, we compared small producers vs. medium producers. For the medium producers, we included companies such as Osisko, B2Gold, and First Majestic, but big producers (majors) were excluded.

Quick data note: we arbitrarily defined small producers as those companies in commercial production with quarterly production below 30,000 oz Au or 1,500,000 oz Ag. Medium producers were any that produced above those benchmarks (but are not considered majors).

Next week, we’ll break down the data even further. First, we’ll look at differences within jurisdictions to see which areas have the most funding from institutions. Then, we’ll see if market capitalization or cash have any relation to either management or fund ownership.

If you haven't already, hop over to Tickerscores.com as we have a free 14-day trial of our service available. It'll give you access to all of our data that we used to compile this article.

It never ceases to amaze me in the junior resource sector just how dumb ‘smart money’ can be.

As with any single quantitative metric, it won’t correlate with success all the time. For example, If you look at only companies that have cash, you can’t use that as the only proxy for them necessarily being smart either. Sure, most companies with cash are doing good things, but some will misallocate the capital on stupid things. That’s why we don’t make investment decisions based on only one metric.

That’s why our system combines 20+ metrics together. A company with high fund ownership, high management ownership, cash, low G&A, and an economic project is likely a better bet than the average company out there. Multiple signs pointing in the right direction = better.

Good answer.