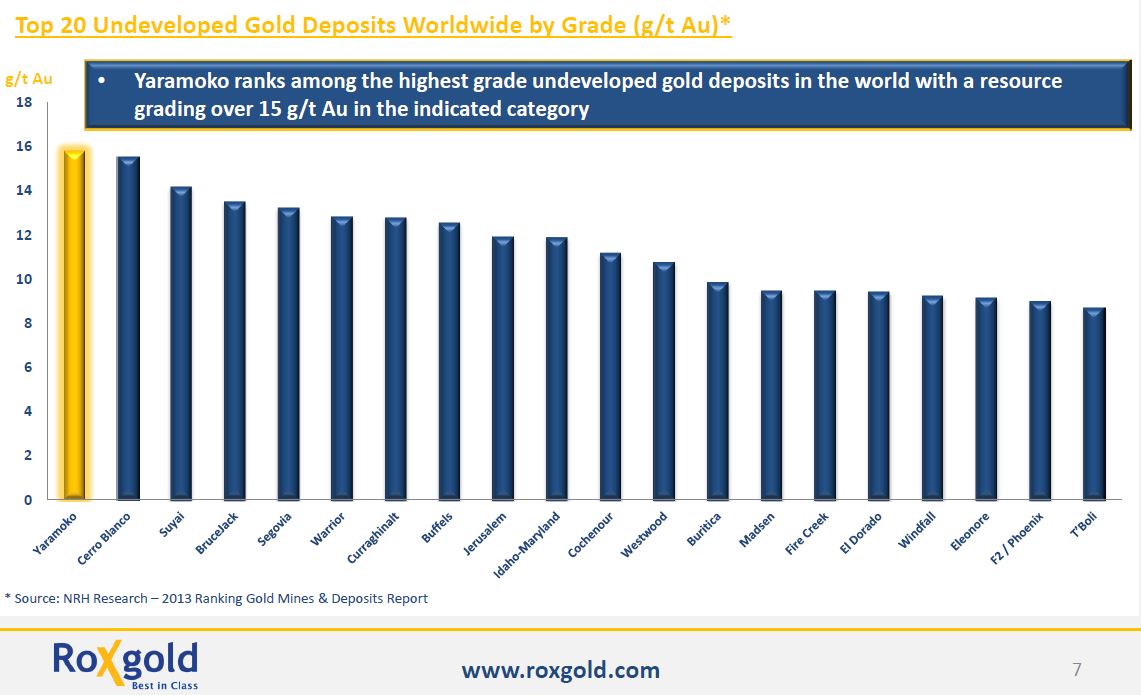

Yaramoko is the highest grade undeveloped gold project in the world (Source: Roxgold)

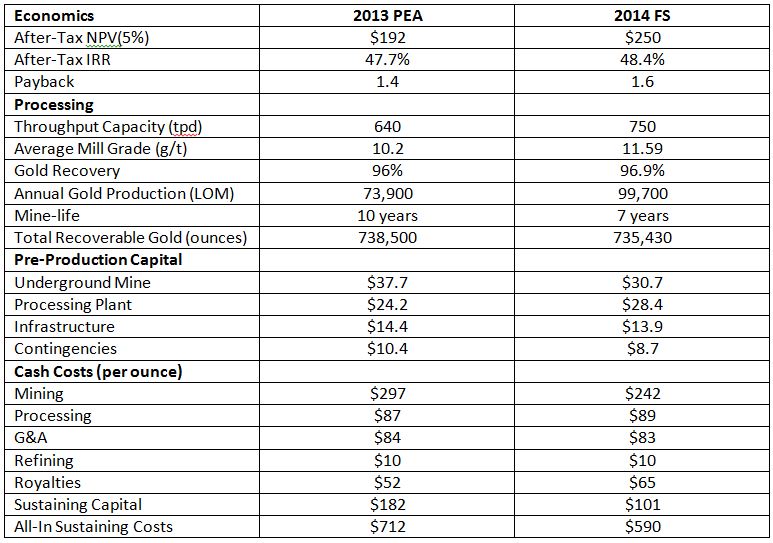

Roxgold (ROG:TSX) which is developing the highest grade undeveloped gold deposit in the world, released their final feasibility study for the Yaramoko project in Burkina Faso. The feasibility study was in line with the company's September 2013 preliminary economic assessment. The company is on track to complete the final stages of permitting in Q3/2014 with underground development starting before year-end.

The largest improvement from the PEA was with regards to the all-in sustaining cost which decreased to $590/oz from $712/oz. This dramatic improvement in operating margin helped increase the after-tax NPV(5%) to $250 million from $192 million. The average grade and recoveries also improved slightly with the average mill grade increasing from 10.2g/t gold to 11.59g/t as well as recoveries increasing from 96% to 96.9%.

The initial capital for the project remains modest at $106.5 million. Roxgold recently completed a $29 million bought deal financing at $0.58/share (included $12.5 million from resource private equity fund Appian Capital) and now the company is sitting on approximately $40 million in cash. The project is economically robust, so I would expect 50-60% of the capex to be finance by debt.

On the conference call, management said they are aiming for $60 million in debt to finance the project. They will have to complete another small piece of equity prior to production.

The company believes it can save $50 per ounce in operating costs related to securing access to grid power as opposed to diesel ($0.45/KWh versus $0.17/KWh). On the conference call, management reaffirmed their confidence that these power contracts will be secured well before production starts.

The project remains open at depth, beyond the 430m extension of the current mine plan. 270,000 ounces of high grade inferred gold resources remain below the 430m depth and extend to 900m. This leaves the project with significant exploration and mine-life extension potential.

Below is an item by item comparison of the 2013 PEA versus 2014 FS:

Click to enlarge (Source: Company Reports, CEO.CA)

The latest mineral resource estimate shows the 55 Zone of the Yaramoko deposit hosting 1.6Mt at 15.8g/t gold in the Indicated category at a 5g/t cut-off which contains 810,000 ounces. Another 840Kt at 10.26g/t gold contains 278,000 ounces in the Inferred category.

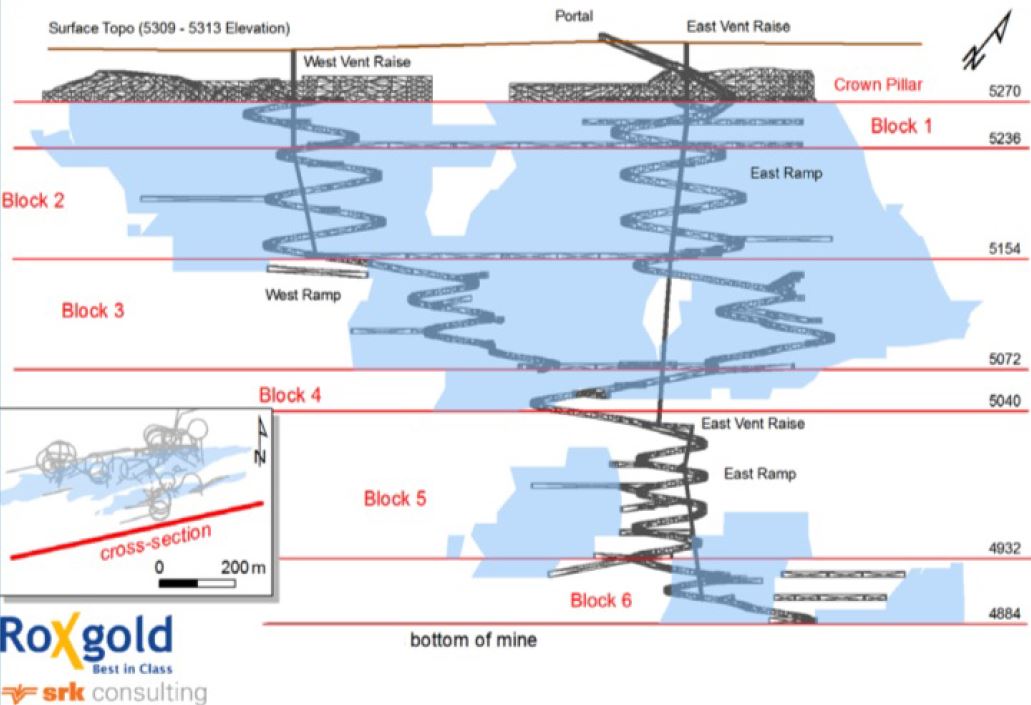

Underground development plan for Yaramoko (Source: Roxgold/SRK)

The mine plan uses a 4.9g/t gold cut-off and a minimum width of 1.6m. The deposit will be accessed from a single decline to the 5270 level where a cross cut will be driven and two spiral declines will access to the 5072 level where another single decline will be driven to a depth of 430 vertical metres (4884 level).

The dual decline in the upper parts of the mine allows for concurrent development of the two declines and doubles the access to open working faces throughout development. Mining will be conducted using long hole retreat mining on close space sublevels, with cemented rock backfill used to eliminate non-recoverable pillars, maximising mining recovery to 96%.

The company is also working to complete studies on paste backfill as opposed to concrete, which management believes could save between $10-$15 per tonne as well as save substantially in sustaining cost related to expanding the tailings ponds later in the mine-life. Roughly 60% of the tailings are solids.

Roxgold shares are up 39% year-to-date and have outperformed the junior gold miner's index (GDXJ) which is up only 11%.

Click here for the Company's presentation.

Roxgold will be hosting a conference call and webcast presentation discussing the results of the Feasibility Study on Tuesday, April 22, at 2:00 p.m. ET.

Conference Call Details:

Toll Free (North America) 888-390-0546

Toronto Local and International 416-764-8688

I do not own Roxgold shares currently, but once done writing I will be building a long position for the following reasons:

- Yaramoko is the highest grade undeveloped gold project in the world

- Low relative capital intensity and excellent all-in sustaining margins

- Valuation is right (cash ~$40 million, EV ~$110 million)

- Strong management and technical team (ex-Fronteer)

- Excellent institutional support (Appian Capital, Sprott, US Global, Van Eck)

Read: Roxgold Announces an After-Tax IRR of 48.4% in Feasibility Study for the Yaramoko Gold Project