This is what all the fighting is about; the Putumayo Basin (Image: Petroamerica Oil Corp.)

After bumping their original share and cash offer for Suroco up 33% (from $0.60 to $0.80 per share), Petroamerica Oil (PTA:TSXV) told investors this morning that their $0.80 offer would be the final one. Suroco's Board is standing by Petroamerica's offer as well.

On April 28th, Petroamerica announced they had reached an agreement with the Board of Suroco Energy (SRN:TSXV) to acquire their company for shares and cash equating to a value of roughly $0.60 per share, representing a 67% premium to their 10-day VWAP. Then, on June 10th, VETRA Holdings (a private Colombian E&P) announced an all-cash bid for Suroco at $0.60 which the Board of Suroco urged investors to reject (at the time, Petroamerica shares had increased and their combined shares and cash offer was valued at over $0.62 per share). VETRA then raised their bid to $0.75 per share and Petroamerica subsequently raised theirs to $0.80 (where it stands today). VETRA's offer now stands at $0.83 per share cash.

Petroamerica's Board is standing by their offer of $0.80 as they believe it is superior given that it is merely 3.75% lower than VETRA's and it allows Suroco shareholders to continue to participate in the upside of their highly prospective Colombian blocks in the Putumayo Basin as well as diversify their profile into the Llanos Basin (Colombia's most productive).

Jeff Boyce, Executive Chairman of Petroamerica, commented: "The Vetra offer should create some doubt amongst the Suroco shareholders. There is too much upside value at stake, especially with the upcoming drilling in the PUT-7 block, for shareholders to sell out for cash at this point. The Vetra offer doesn't allow Suroco shareholders to participate and share in the substantial potential upside of the N Sand oil play. This further begs the question -- what else could Vetra know about the Suroco assets? For this reason, Petroamerica is offering shareholders of the combined company the opportunity to participate in expected significant equity value appreciation over the next couple of years."

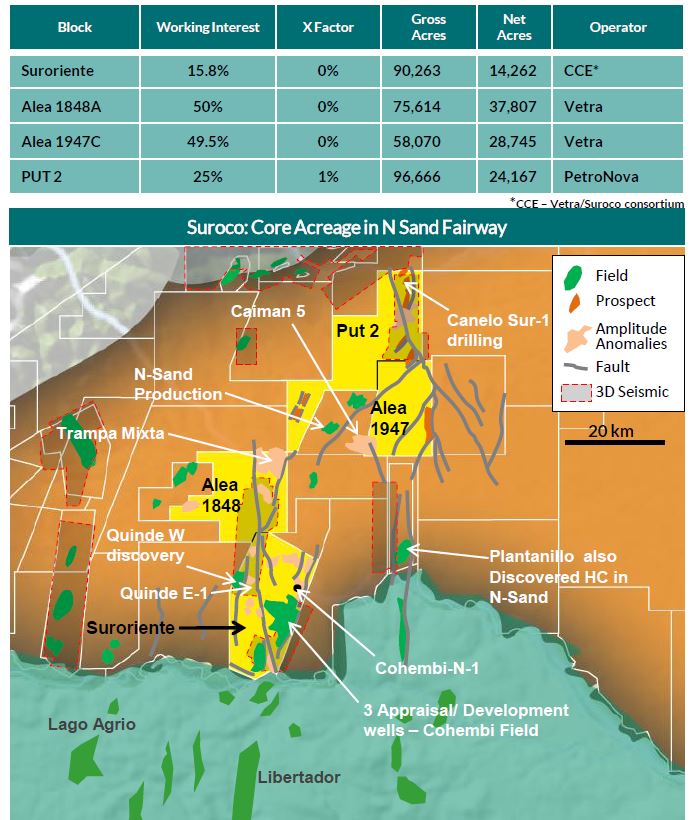

Given how prospective their PUT-7 block is, it would be the height of stupidity, as a Suroco shareholder, to tender your shares to VETRA (in my opinion) for $0.03 per share more in cash. The 3.6% discount you pay for accepting the Petroamerica offer is the price of admission to continue to participate in the upside of the N Sands oil play.

Ralph Gillcrist, COO and VP Ex, commented: "We believe we can unlock tremendous future value for the combined company from the N Sand oil play. For example, based on our internal estimates, a 20-million-barrel oil discovery in the PUT-7 block could easily deliver over $250-million in after-tax net present value, discounted at 10 per cent, to the combined company, which, based on current market multiples, implies a return of over 100 per cent for Suroco shareholders to the Vetra offer. We have structured our offer so that Suroco and Petroamerica shareholders can jointly participate in this considerable reserve growth and value creation we envision."

In the release, management highlights the fact that "research analyst's target prices for Petroamerica imply $0.98 per Suroco share of potential value to Suroco shareholders."

Jeff Boyce, Petroamerica's Chairman founded a number of oil and gas companies including Vermillion Resources (now a $4 billion company)

Add to that the fact that VETRA's offer has fine print in it which muddies their offer. Included in the fine print is a condition that states: "there is to be no material adverse change as a consequence of taking up and paying for Suroco common shares under the VETRA offer." Acquiring Suroco would, in all likelihood, trigger a repayment clause in their existing debt which would make $23.5 million immediately payable. That sounds fairly materially adverse.

Petroamerica's Board has a clear plan for unlocking value in Suroco's assets and sharing that value with existing Suroco shareholders. They envision a combined company with a 5 year reserve life and 30,000boe/d of production within three years. With that type of average production that would be a company generating close to $500 million in average annual operating cash flow (assuming $40/barrel operating netbacks). Note, Petroamerica's operating netbacks over 2013 averaged $75 per barrel.

That's not just talk either, Petroamerica has continued to consistently deliver on their production guidance. This management team has already grown the company's production from 512boe/d at the end of 2011 to 6,478boe/d in the first quarter of this year (over 1,165% growth).

To put that in context, Parex Resources produced an average of 18,425boe/d from their Colombian asset base. Parex trades at a $1.6 billion valuation ($87,000 per flowing barrel). The combined market capitalization of Suroco and Petroamerica is roughly $300 million (simple addition). Petroamerica trades at $30,000 per flowing barrel.

Suroco shareholders will vote at the Annual and Special Meeting on Monday, June 30, 2014 at 8:00am MDT (Calgary local time).

View Petroamerica's presentation outlining their rationale HERE.

Disclosure: I am long and biased. Due your own due diligence.