Integra's acquisition is accretive on all metrics (Image: Integra Gold)

After remaining halted for most of the trading day yesterday, Integra Gold (ICG:TSXV) announced that it made a timely and accretive asset acquisition which includes a fully-permitted 2,200tpd mill and tailings facility.

Critically for Integra is key underground infrastructure which will allow the company to access their deposit from underground enabling them to drill from underground as well as access the main part of their ore body without having to sink this expensive infrastructure themselves.

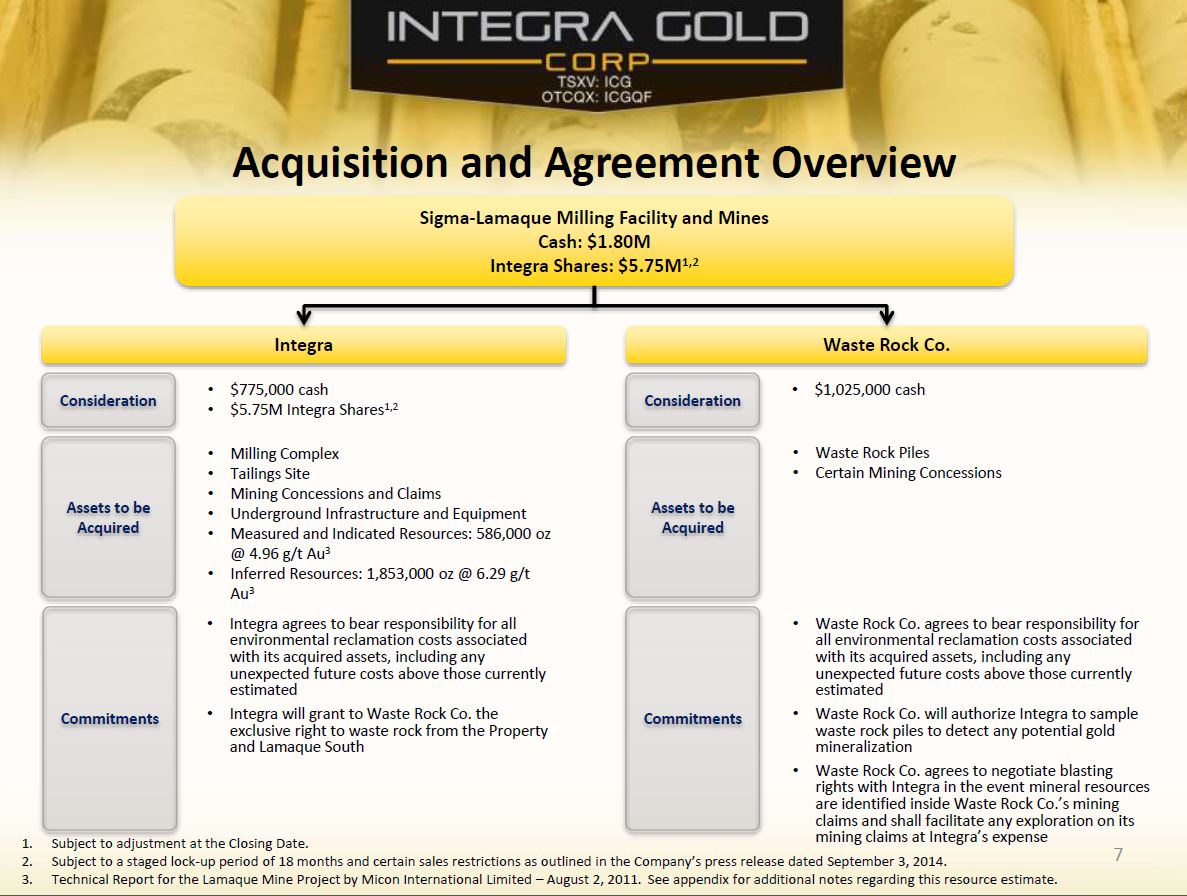

Integra announced that it would be acquiring the historic Sigma-Lamaque mining complex which is directly adjacent to their own Lamaque South project. The Sigma-Lamaque complex has been in receivership since 2012 after being owned by Century Mining.

This complex has been valued by WSP Canada Inc. (a reputable Canadian engineering firm) at over $100 million and that is exclusive of the gold resource which are currently there as well. The purchase price for Integra is just a small fraction of that; $7.55 million. What's even better is that after some clever deal making, the company's net cash outlay is only $755,000 after they brought in a third part waste rock company for most of the upfront cash payment.

The purchase price consists of $1.8 million cash and 25 million shares valued at $5.75 million (based on $0.23/share price).

Simultaneously, the company has entered into an agreement with a construction materials and mining company known as the Waste Rock Company (WRC) which will get ownership of the historic waste rock inventory at the Sigma-Lamaque mine and some non-core mining concessions. In exchange, this third party ground will pay Integra $1.025 million which is, in turn, being used to pay the $1.8 million upfront cash payment.

The asset is a permitted 2,200tpd milling complex and tailings facility which is 500 metres from the Lamaque South project. Although the mine has been on standby since May 2012, the company claims the infrastructure is in excellent condition and has been well maintained. The tailings facility currently has up to three years capacity with room for expansion after that.

The underground infrastructure is also fully-permitted and includes three portals, mechanical shop, office and equipment.

Due to the fact this project was an old operating mine, there are liability and environmental concerns. Integra brought in a third party engineering firm to evaluate the potential future liability and they determined that $12.1 million worth of future reclamation would be necessary.

After removing the waste rock (which WRC will be taking to make roads, etc), Integra estimates their future obligation to be $5 million of which $3.5 million is already paid for by a pre-existing reclamation bond held by the Quebec government. The remaining $2.5 million in estimated future liability will be split by Integra and WRC.

(Image: Integra Gold)

I had been watching the Sigma-Lamaque complex in receivership for sometime now, but there were only so many mining companies that it would make sense for and Integra was the obvious number one choice.

Any way you cut it, Integra is getting the mill, tailings and associated infrastructure on extremely cheap metrics.

Under Integra's current PEA, the company had budgeted $46 per tonne for toll-milling and transportation, including a $15 per tonne toll surcharge. This is now eliminated which will dramatically improve operating costs and margins per ounce.

On top of these operating savings, the company also improved their capex (currently estimated at $69 million) by acquiring offices, water management systems, shops and most critically key underground access routes.

Integra Gold has already caught the attention of a lot of investors, but now will likely start to catch a bid from the broader markets as the company represents one of very few gold mining companies developing a new high-grade gold mine in Val d'Or. Also, this acquisition de-risks them from a development perspective in multiple ways. Metallurgical questions are answered given Sigma-Lamaque's history. Capex questions are answered. Operating costs and toll milling contract concerns are removed.

This acquisition essentially catapults the company into the late-stage development category and, as a result, should see the share price continue to re-rate.

The company has already been able to attract five research analysts and will now, likely, attract more as this story truly starts to take shape now.

They still have a number of key catalysts upcoming, including:

- Ongoing drill results (Q3/2014)

- Updated resource estimate (Q4/2014)

- Permitting (H1/2015)

- Updated economic study to incorporate newly acquired mill and infrastructure (H2/2015)

Shares are up nearly $0.065 or 26% to $0.31 per share at the time of writing.

In June, the company set out to raise a bit of cash to allow them to continue to drilling. They intended to raise $4 million, but were inundated with orders and ended up closing just over $10 million a few weeks later.

Integra will hold a conference call and webcast on Thursday, September 4th at 7:00 am PST/10:00 am EST to discuss the proposed acquisition.

- A live audio webcast will be available at www.accuconference.com/join (Log-In: 1.800.868.1837; Conference Code: 346621).

- Participants may also join the conference by calling 1.800.868.1837 (Conference Code: 346621#) or 1.404.920.6440.

- To listen to a recorded playback of the call after the event, please call 1-800-920-7487 (Conference Code: *346621#] in North America.

Read: Integra Gold to Acquire Sigma-Lamaque Milling Facility and Mine

Disclosure: Integra Gold is a client. I am not a shareholder, yet. Always do your own due diligence. Thank you