Investors have long been trained to think that when it comes to gold, deflation is bearish and inflation is bullish. This basic economic theory holds that during inflationary periods the value of paper currency declines (less purchasing power) with every passing day, whereas gold maintains its purchasing power (hence the phrase "store of value") and appreciates in terms of the inflating currency. During periods of deflation money is tight and prices of goods & services actually decline as the value of currency increases. Gold in turn depreciates in terms of the appreciating currency.

However, for a number of reasons (central bank interventions, globalization, currency unions, etc.) the traditional definitions of inflation and deflation are not necessarily applicable to the current macroeconomic landscape. Moreover, central bank policy responses to prevailing economic conditions have drastically changed how investors may react during bouts of deflation/inflation.

During the 2008-2009 Global Financial Crisis (GFC) a severe threat of deflation caused global central banks to implement extraordinary policy accommodations in order to loosen financial conditions and halt the economic hemorrhaging. The unknown consequences of quantitative easing (QE) and ZIRP (zero interest rate policy) prompted investors to rush, en masse, into precious metals over the ensuing years:

Gold nearly tripled in less than 3 years between 2008-2011

It's clear that the marginal buyer/seller in the gold market is the investor i.e. jewelry demand did not push the price to $1923 in 2011 and producer hedging didn't trigger the April 2013 gold crash. As was noted above investors have been trained to buy gold during times of inflation or when they perceive that an inflation threat is around the corner. This happened in the past decade, as investors bought gold when they perceived that central bank inflation programs were the only solution to the debt deflation bust generated by the GFC. And recently it happened again as investors decided to sell gold when they perceived that inflation was not a threat and that Fed policy accommodation was fast approaching an end.

While elevated levels of inflation have not materialized in developed economies recently, to state that this recent phenomenon negates the investment case for gold misses the point entirely. Central banks (ECB, Fed, BoJ, etc.) continue to be laser focused on combating disinflationary pressures and the much more dire possibility of deflation. Each time disinflationary pressures have kicked up in the past decade the Fed and other central banks have been there ready to kickoff a fresh stimulus program (inflation program).

What is the endgame of all this extraordinary monetary policy accommodation? Nobody knows. However, a couple of things are pretty clear: first, the global central banks aren't done, and second, the threat of deflation is as strong as it has ever been.

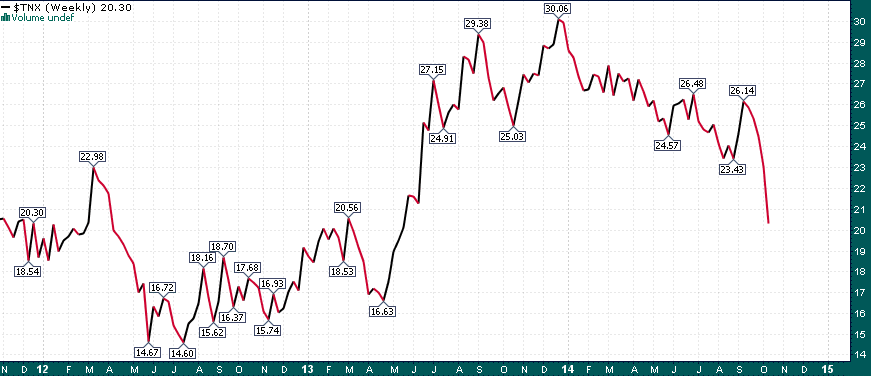

Falling bond yields and weak economic growth signal that disinflation/deflation are still very real threats:

US 10-year Treasury Note Yield

Leading Economic Indicators

If history is any indication, the Fed and other global central banks will be quick to step in with additional stimulus measures if the above trends persist much longer. A scenario may transpire in which inflation rates in developed economies hit zero and begin to turn negative even as central banks open up the liquidity spigots anew. Under such a scenario, deflation or at least the threat of it, is likely to be very bullish for gold.