In a recent Ernst & Young study measuring business risks faced by mining companies, capital dilemmas, social license to operate, resource nationalism, and infrastructure access all ranked in the top ten.

Integra Gold (ICG:TSXV), a junior Canadian gold developer, recently completed an innovative and transformative acquisition that has removed all of the above risks from their growing Quebec gold camp.

Integra holds a portfolio of high-grade gold deposits in Val d’Or (literally, “valley of gold”) in Quebec, Canada. Over 130,000 metres of drilling in the last 3 years has defined a 1-million-plus ounce gold deposit, indicated and inferred, with grades averaging 7.1 grams per tonne (g/t) gold, putting the Lamaque South project in the top quartile by grade of undeveloped gold deposits globally.

Recently we had a chance to sit down with Stephen de Jong, the young leader of the company. Since taking over as President and CEO in July 2012, he has raised over $25 million, increased the company’s mineral resource inventory by over 300% and completed a preliminary economic assessment (PEA) that highlighted a low capital intensity project with robust economics.

Perhaps the most impressive move by the 31-year-old de Jong was his most recent: the acquisition of the historic Sigma and Lamaque mining complex adjacent to Integra’s existing Lamaque South project. The complex includes, among other things, a fully functional and permitted 2,200 tonnes per day (tpd) mill and significant underground mining infrastructure, not to mention over 2 million additional ounces of high-grade gold resources (Measured, Indicated and Inferred).

To understand the significance of the acquisition and how it propelled the company to the next level, it is probably useful to outline each part of the now combined entity.

Aerial map highlighting why Integra was the only company capable of cutting a deal on the Sigma-Lamaque complex (Image: Integra Gold Corp.)

Lamaque South (1)

Integra has been working on developing the Lamaque South project in which they delineated a 3.3 million tonne deposit at an average grade of 7.1 g/t gold, with 756,280 ounces of gold in the Indicated category. A March 2014 PEA outlined a room-and-pillar and long-hole underground mining operation accessed by two ramps with the majority of production coming from two main zones; the Parallel and Triangle zones.

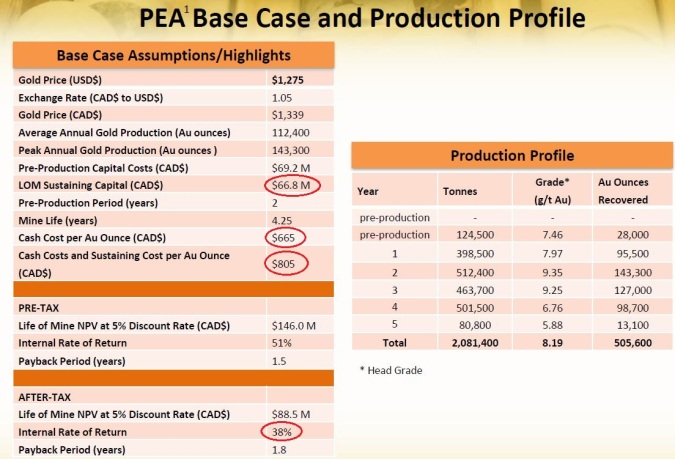

The PEA envisages a mine producing an average of 112,400 ounces of gold annually over a 4.25 year mine-life with peak production in year 2 of 143,300 ounces. Average cash costs were estimated at $665 per ounce with all-in per ounce costs of $805. Based on $1,275 per ounce gold, the Lamaque South mine should generate an after-tax NPV (5%) of $88.5 million, IRR of 38% and pay back the $69-million initial capex within 1.8 years (note, the estimated capex is netted of pre-production revenue from 28,000 ounces of production during year 2 of construction).

A few takeaways from the PEA:

1. The PEA assumes a toll milling operation whereby the company would truck ore to nearby mills for processing. This would add $15 to $20 per tonne to Integra’s operating cost profile for transportation, but would eliminate tens of millions of dollars of initial capex that would otherwise be necessary for the construction of their own processing facility.

2. The mine life is short, but is typical of narrow vein mining in the area where mines would ultimately produce millions of ounces of gold over multiple decades of production, but at any given time would have short reserve lives (typically 3 years).

3. The resource model only assumes mineralization to a total vertical depth of approximately 600 metres even though the deposit remains open at depth and the neighbouring Sigma and Lamaque deposits were mined to depths in excess of 2,000 metres.

The Sigma-Lamaque Mill and Mine (1)

The Sigma-Lamaque property is comprised of the former Sigma (Placer Dome) and Lamaque (Teck Cominco) underground mines, each of which have over 80 years of operating history and collectively produced over 9.4 million ounces of gold. The property is located immediately adjacent and to the north of Integra’s Lamaque South property.

The Sigma and Lamaque mines were consolidated under Placer Dome in 1993. Since Placer Dome's ownership there have been various owners, most recently Century Mining which operated there between 2004 and 2012. The property has been on care and maintenance since an immense debt load forced Century into bankruptcy in 2012.

The Sigma-Lamaque project has a fully permitted processing facility capable of processing 2,200 tpd and includes crushing/grinding equipment and a gravity circuit.

The deposit also hosts 3.7 million tonnes of material at an average grade of 4.96 g/t gold containing 586,000 ounces in the Measured and Indicated categories, with an additional 1.85 million ounces in the Inferred category (9.2 million tonnes at an average grade of 6.29 g/t gold).

Mr. de Jong says the mill complex at the Sigma project is in excellent shape as it has been on an extensive care and maintenance program since it closed in 2012. Historic gold recoveries in excess of 95% have been reported from the mining circuit. Additionally, the circuit has been proven with essentially the same ore that Integra has at its Lamaque South project, so similar types of high recovery rates should be achievable.

The project is fully permitted with service portals and underground workings close to the Parallel Zone at Lamaque South, providing potential quick and cost-effective access to the mineralization there.

Most recently, the company announced that after reviewing the project description for the combined Sigma-Lamaque complex and Lamaque South project, the Canadian Environmental Assessment Agency determined that Integra will not have to file an onerous and time-consuming Environmental Impact Statement. This potentially shaves up to 9 months off their development timeline.

The reason for this decision by the Canadian authorities is that the Sigma-Lamaque mine and mill are already permitted and the Lamaque South part of the project will disrupt very little in terms of surface and underground development, given that Integra plans to utilize as much of the existing infrastructure as possible.

The Sigma-Lamaque mill facility includes a fully functional 2,200tpd mill circuit including: crushing, grinding, CIL and pulp, etc. (Image: Integra Gold Corp.)

There are a few takeaways from the Sigma-Lamaque Mill and Mine deal:

1. The town of Val d’Or exists as a result of this mining complex and so the town and labour force there is pro-mining. Additionally, significant human capital in terms of skilled underground miners is available in the town.

2. The flow sheet of the Sigma mill is the same as contemplated for the stand-alone Lamaque South mine and so no new processes will be introduced, keeping the technical risk low.

3. The Lamaque South deposit is believed to host very similar mineralization to the Lamaque and Sigma deposits for which they already have extensive metallurgical data as a result of being in production for over six decades.

4. Due to the fact that the Sigma and Lamaque mines have been in production for so long, mining stopped at 2,000 metres and 1,000 metres, respectively. This provides unique underground access for Integra’s neighbouring Lamaque South deposit.

5. Existing underground infrastructure will be used to access the Parallel Zone, potentially decreasing the timeline to production. A portal from surface at the Parallel Zone will no longer be necessary.

6. With the Sigma-Lamaque complex already permitted, the Lamaque South project no longer requires its own Environmental Impact Assessment which speeds up the time to production and ultimately cash flows.

The Consolidated Play: 1 + 1 = 3

As mentioned earlier, the Sigma-Lamaque complex has been in receivership since May 2012, when previous owner Century Mining went bankrupt.

This has provided a unique opportunity for neighbouring Integra Gold, which had already drilled and defined a high-grade gold ore body next door. Opportunity seized: owning the extensive mill, tailings facility, etc. creates a consolidated gold play with well-defined high-grade gold mineralization and existing permits and infrastructure to expedite its development.

One potential pitfall of the stalled Sigma-Lamaque complex was a significant environmental liability in the form of old waste-rock piles.

When they were looking at a potential consolidation, Integra hired a well-known third-party engineering firm to assess the dollar value of the liability, which was subsequently estimated to be $12.1 million.

Enter Mr. de Jong and his team, who devised a creative and accretive acquisition plan that would not only see Integra deal with the liability, but also profit from it.

To get around the full $12.1-million environmental liability, Integra found a contractor (Fournier et Filis) that could use waste rock for aggregate in road construction and other industrial purposes. Not only will Fournier now assume the majority of the waste rock liability, but they will actually pay cash for it.

Of the total estimated future liability, the removal of the waste rock piles immediately eliminates roughly $7.1 million of future costs. A $3.5-million reclamation bond was already in place so Integra’s ‘all-in’ liability exposure has been reduced to just $2.5 million (after giving $1 million of the bond to their Fournier).

In the end, Integra will pay a total of $8 million in cash and stock for the asset. What’s even better is that of the $8 million, Integra will only be out of pocket $775,000 cash. That’s because Fournier has agreed to pay Integra $1.025 million for the waste rock pile.

This is a fraction of the $100-million replacement value WSP Canada (an independent engineering and consulting firm) assigned to the mining complex; a number which excludes the gold resources.

The remaining acquisition price will be completed by issuing roughly 25 million ICG shares at a deemed issuance price of $0.25 per share, representing minimal dilution (approximately 13%).

What does it all mean?

Red are just a few areas that are likely to be improved with the acquisition (Image: Integra Gold Corp.)

Recall the ranked business risks faced by mining executives: capital dilemmas, social license to operate, resource nationalism and infrastructure access. With the acquisition of the Sigma-Lamaque complex, Integra’s risk profile is significantly lowered on all of those fronts and more.

1. Capital dilemmas (aka financing risk): With the acquisition, operating cost savings of up to $20 per tonne will be instantly achieved by eliminating the trucking requirement and toll milling fees that were envisaged in the PEA under a toll milling scenario. This will provide greater operating margins and thus a more resilient project in a falling gold price environment. This should ultimately help reduce Integra’s cost of development capital as well.

2. Social license to operate/resource nationalism: Quebec was ranked as the 11th best mining jurisdiction by the Fraser Institute’s 2013 survey. Val d’Or, founded on the back of mines and full of generational underground miners, is an excellent example of Quebec’s pro-mining culture.

3. Infrastructure access: This is perhaps the most obvious and quantifiable benefit of the acquisition. Not only does it allow the company to lower its operating costs by eliminating toll milling, but it also reduces the total upfront capital requirement by providing substantial underground workings (tunnels, shafts, drifts, etc.) as well as access portals from surface. The dollar amount of capex savings isn’t clear yet, but the company believes that they will be able to access the gold quicker by eliminating the need for underground access tunnel and portal developments.

Risks

The primary risk facing Integra shareholders, and one that was brought on by the acquisition of the Sigma-Lamaque complex, is the issuance of 25 million shares into the hands of a court-appointed receiver. As you can imagine, these are not strong hands. Under the terms of the acquisition, the shares are subject to a staged 18-month lock-up, with one third of the shares saleable every six months and the first tranche open to the market on April 8, 2015. The company has inserted some language into the deal terms giving Integra the right to try and find a buyer for those shares prior to any disposition in the open market.

With almost all development companies today, financing risk is a top concern. Capital for development projects (especially gold projects) is especially hard to come by, with even the best management teams having to take on dilution in order to move their projects forward. Integra’s capex is very manageable especially when compared to its cash flow generation capacity.

As far as other risks go, like any mining company the price of the underlying commodity is one of the biggest value drivers. That being said, with the elimination of toll mining and the associated cost savings, the project’s operating margins should improve in the updated mine plan.

Conclusion

Overall, Integra Gold continues to offer investors what it always has: high-grade gold in a world-class jurisdiction. With the acquisition of the neighbouring Sigma-Lamaque complex, Integra now offers investors high-grade, near-term gold production with one of the lowest price-tags in the industry.

The synergies gained from the acquisition are almost immeasurable. Integra benefits from the fact that the only acquirer that makes sense for the Sigma-Lamaque complex is Integra.

With the intensity of the Osisko bidding war, the market has become aware of how valuable high-quality mining projects in safe jurisdictions are. I wouldn’t expect this trend to continue, and that puts Integra in a unique position; one in which investors could pay a premium for their shares, either as an economic and stable gold producer and/or as a takeover target.

Upcoming Catalysts:

1. Exploration drilling, 15,000 metres (Q4/2014)

2. Updated PEA, with detailed integration of the Sigma-Lamaque complex (Q4/2014)

3. Updated resource estimate for Lamaque South deposits (Q1/2015)

4. Updated mine plan with Sigma-Lamaque complex integrated (Q1/2015)

Symbol: ICG.TSXV

Share Price: $0.20

Shares O/S: 185,615,698

Shares F/D: 248,773,249

Market Capitalization: $37 million

Working Capital: $6 million

For more information visit www.integragold.com and add ICG.TSXV to your watch list.

Disclosure: Integra Gold Corp. is a CEO.ca client. All facts are to be verified by the reader. Always do your own due diligence as this is not investment advice (please see full disclaimer).

Big congratulations to Steve de Jong! Keep up the hustle big guy.

This is great. One of the few good ones out there. Much respect to their whole team.