I had to shake my head while reading news from International Tower Hill Mines (ITH.T) this morning that they successfully closed an $8.4 million financing. The investors who bought this financing are throwing money away in my humble opinion.

On July 23rd, 2013 International Tower Hill released the Feasibility Study on the Livengood Project.

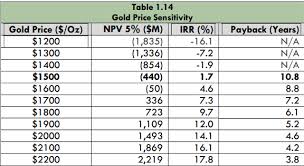

Let's take a look at economics of the project.

- A $2.79 billion dollar CAPEX and an additional $667 million is sustaining CAPEX.

- At $1,500/oz gold the project generates an IRR of 1.7%.

- At $2,200/oz gold the project IRR is now 17.1%

You could argue investors are getting tremendous leverage as a 'cheap' call option on the gold price but in my opinion even that argument makes little sense.

Does this look like a mine that will get built anytime soon?

Heck no.... from those economics you would need to see gold well above $2,000/oz to even think about it.

The project is simply too big, too low grade, and has a CAPEX that makes it uneconomic probably even for the next gold bull market cycle.

International Tower Hill after closing the financing now has ~$15 million in working capital. The plan for the money is to try and optimize the economics of the project (decrease capex, opex, while maintaining strong production profile...pretty tough given the infrastructure needed and the grade of the deposit). They will need to do something magical to get this project optimized to be built anytime soon.

If the recent financiers read this post please contact email me (james@ceo.ca) as I have dozens of projects in mind that can generate significantly better returns.

Do you have any comments on ITH or the stupidy of mining investors? Please feel free to comment below.