Drills turning at Roxgold's Yaramoko mine site in Burkina Faso (Image: Roxgold Inc.)

Shares in Roxgold (ROG.TSX) are up 20% already this year and 35% from their tax-loss influenced low of CAD $0.48 per share in mid-December.

This morning, I spoke with John Dorward, President and CEO of Roxgold who was in Burkina Faso last week meeting with the newly appointed Minister of Mines and getting his new General Manager, veteran underground mining engineer Iain Cox, accustomed to his new digs.

Dorward joined the company in 2012 after the current Chairman, Oliver Lennox-King, won a battle for control of the company and appointed Dorward to lead the new efforts. Since then, he has raised over US $80 million in equity for the company and advanced the project through feasibility and permitting (almost).

"It's all systems go," Mr. Dorward told me by phone from Roxgold's Toronto headquarters.

The company is gearing up for a 12 month build-out of their 750 tonnes per day Yaramoko mine which is expected to produce 120,000 ounces of gold in its first full year of production (2016) at an average all-in cost of less than US $590 per ounce.

The company is waiting on a final signature for their exploitation permit which they expect imminently.

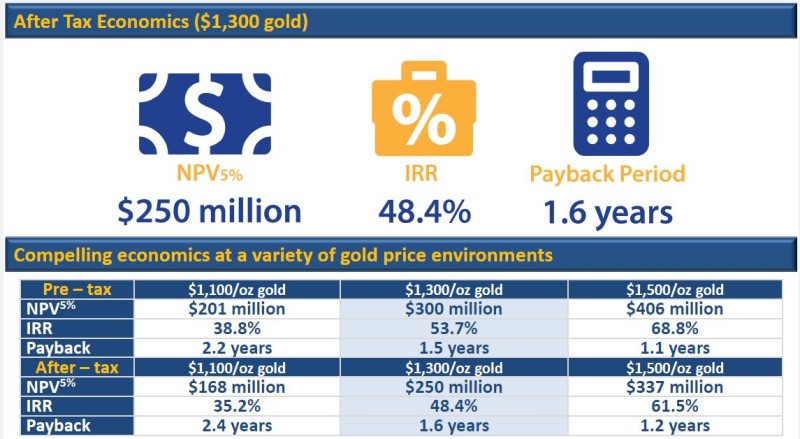

Assuming gold is trading roughly at today's spot price early next year, that translates to US $76.8 million (roughly $91 million in CAD dollars) in first year cash flow from the mine. The current market cap less cash is approximately CAD $150 million.

Roxgold's Yaramoko project remains one of the most economic development-stage gold assets in the world (Source: Roxgold Inc.)

In previous cycles, investors were willing to pay for production that was 18-24 months in the future. In today's market, these companies aren't even getting paid for production that is already paid for and is only one year away.

This phenomenon is not unique to Roxgold and is especially true for the West African miners. See True Gold Mining or Asanko Gold (AKG.TSX) who are both slated to produce high-margin ounces in less than 18 months and who are both fully-funded, but who are also trading near the cash flow they will generate in the first year of annual production (at spot prices).

Roxgold is coming off a turbulent end of 2014 with a quasi-coup d'état in Burkina Faso sending investors of West African miners to the exits.

Then, at the end of the year, their co-lead arranger on a US $75 million project finance debt facility, Credit Suisse announced they would be bailing on their half of the deal.

"We could see the writing on the wall," Mr. Dorward explains. "They announced they were leaving the commodities finance business last year and that wasn't a good sign."

The reality is that Credit Suisse's departure from the deal, although ill-timed, had less to do with the company's ultra high-grade Yaramoko project or Burkina's recent political strife and more to do with the fact they aren't committed to this business unit going forward.

Having Societe Generale (SocGen) remain committed to the project and the finance facility should give investors confidence. SocGen has a big presence in West Africa and actually has a local branch in Burkina. Importantly, SocGen recommitted to the previously agreed to terms of LIBOR +4.25-4.75%.

Mr. Dorward says they are in advanced talks with a number of lenders, most of which are in the credit approval-stage which means the project has passed technical due diligence (no surprise here). Many of the lenders were part of the first bid process and so the due diligence has moved quickly Mr. Dorward told me.

With the dissolution of the old and installation of a new Burkina government, the signing of an official State Decree, which is the final document that needs the Ministry's signature, has been slightly delayed. Mr. Dorward believes his first meeting with Burkina's new Minister of Mines was very positive.

"The message we got was that the Decree is on track and is basically 'in the mail'," says Mr. Dorward although he cautioned saying that the Minister wouldn't provide any dates for when the company could expect to receive a final signed Decree.

"It's basically business as usual in Burkina," he says. "The government remains very committed to mining."

Despite the delay, the company is still guiding an end of 2015 mine start-up with full production commencing in late Q1/2016.

Management believes they can still achieve this timeline (assuming they receive the Decree shortly). They will then be able to move ahead with the construction of the camp and other big ticket items with the current cash on hand (US $42 million) while the debt facility paperwork is finalized.

Once the debt package is in hand, the project's US $106.5 million price-tag will be fully accounted for.

Roxgold has already completed the detailed engineering and design, manufacturing of the SAG mill is 60% complete, long lead items for the power line are 40% complete and the early works contracts have been advanced and are just pending the receipt of the Decree.

Additionally, the company is actively exploring regional targets including the Bagassi South zone which currently has assays pending.

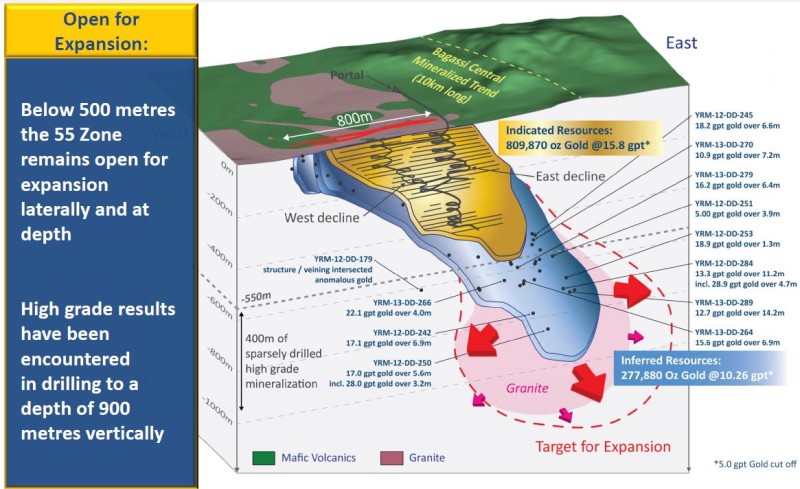

The high-grade 55 Zone deposit remains open at depth below 500 metres with drilling to 900 metres vertical depth still hitting high-grade gold (Source: Roxgold Inc.)

"Ultimately, it comes down to the fact that Yaramoko is a truly unique project. it will get financed and will be built," Dorward said.

By all accounts Yaramoko is a world-class deposit and as such will likely be a company both investors and corporates pay close attention to going forward.

With its average head-grade of 11.59 g/t gold and all-in operating margin of US $640 per ounce (based on US $1,230 per ounce spot) combined with its 100,000 ounce per year production profile, Yaramoko is a likely takeover candidate.

1/3rd of the company's shares are owned across three funds and the Chairman (Oliver Lennox-King) so a deal would likely come by way of friendly offer and at a much higher share price than the company is currently trading at.

(Note, according to SEDI filings Appian Capital is the largest shareholder and bought 21.5 million shares at $0.58 and another 12 million at $0.65. They acquired an additional 11 million shares out of the market last year at prices between $0.61 and $0.70 per share. They hold 6 million warrants at an exercise price of $0.90).

Mr. Dorward and Roxgold will be spending a lot of time of the road over the next few months.

They will be in Vancouver this weekend for the 20th annual Vancouver Resource Investment Conference held by Cambridge House (register HERE). They will be at booth 1727 and will be giving a presentation at 1:30pm on Sunday January 17 in Workshop 3.

Read: Roxgold Provides Financing and Project Development Update

Related: This Gold Developer Punches Above Its Weight (John Dorward Interview)

Author owns shares of Roxgold and as a result is biased. This is not investment advice. Always do your own due diligence.

Roxgold, Reservoir, Pretium, Midway, Detour, all good M&A targets…each umique in its own way with good either a good partner, a good project, a good political jurisdiction, good balance sheet, good……..