A mining shovel at the Detour Lake mine (Image: Detour Gold)

Detour Gold (DGC.T), the owner of one of Canada's largest producing mines, released 2014 year end results and guidance for 2015 this morning. Detour is still in the process of trying to increase the milling rate and therefore output at the mine.

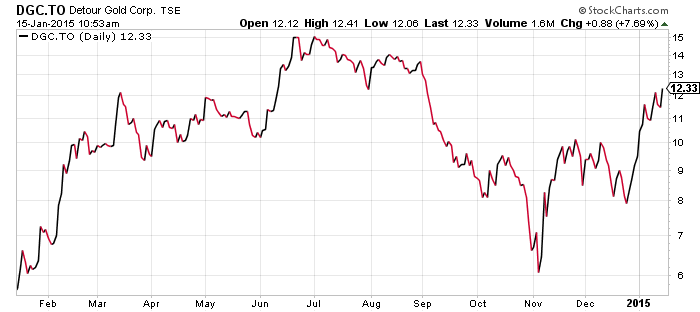

The stock is up 8% at press time but I believe the majority of that is from the bump in gold this morning rather than the yearly results. Detour is highly leveraged to the price of gold as it is a large producer with higher costs mostly due to the average grade being mined of ~0.80 grams per tonne.

2014 saw the company take a big step in the right directing with production of 456,634 ounces which was a 97% year over year increase from 2013 production of 232,287 ounces.

2015 guidance is between 475,000 and 525,000 ounces at an all in sustaining cost of $1050-$1150 per ounce.

Highlights for 2014 include

- Gold production of 456,634 ounces, achieving lower end of guidance

- Preliminary total cash cost of $930 per ounce sold, at midpoint of guidance; with fourth quarter estimated total cash costs of $875 per ounce sold

- Exited 2014 at an average mill throughput rate of 54,310 tonnes per day (tpd) and mining rate of 234,000 tpd for December

Paul Martin, president and chief executive officer, commented: "We are pleased to announce that we achieved our production and cost guidance for 2014 and ended the year with $135-million in cash and short-term investments. By year-end, the mill was performing within 1 per cent of design capacity and mining rates were improving with an average of 234,000 tpd in December. Building upon this momentum is our key priority for 2015. We are optimistic that the initiatives we have under way, including improvements in the mining rate and the potential of processing of fines from our stockpiles, can further enhance our 2015 performance and enable us to achieve the higher end of our production guidance and lower end of our total cash cost guidance."

Detour share price responded in 2014 by doubling year over year as production increased.

I listened in on the companies conference call this morning to get the latest for CEO.ca readers.

Two interesting things I learned from the call involve costs savings from the weak $CAN dollar and the lower diesel price.

- Every 1 cent drop in the dollar adds approximately $4 million to the Detour bottom line in year.

- Detour uses 45-50 million litres of diesel per year so a 10% decline in the diesel price would also add approximately $4 million to the bottom line annually.

I still believe Detour is a legitimate takeover in the gold space as I mentioned in this post. Any company in the market for a large asset with a long mine life must have Detour near the top of the list.

With a market cap of ~$2 billion Detour is still trading at nearly half of the $3.9 billion dollar valuation Osisko received last year.

Symbol: DGC.T

Share price: $12.47

Shares outstanding: 157. 87 M

Market cap: $2B

Read: Detour Gold Reports Fourth Quarter and Full Year 2014 Operating Results and Provides 2015 Guidance or Goldcorp's next takeout

Discuss here in CEO.ca chat here

I have no position in any of the stocks mentioned. This is not investment advice. All facts are to be verified by reader.As always please do your own due diligence

Large asset, long mine life, room for growth/grade, strong fundamentals (costs culd be lower), good jurisdiction, good management, leveraged to commodity price, etc… makes DGC a strong takeover candidate; however, the share price already has some of this ‘takeover’ speculation baked into its price, so I don’t think the premium will be as rich as most ppl expect

– Always PTHYD