Over the past five years zinc bulls have gone nowhere. However, the metal, used primarily for galvanizing steel in the construction industry, is setting up for a substantial supply deficit as early as next year which could see the spot price pop.

Investors interested in the zinc space have very few investable options.

The majority of zinc outside of China is produced by majors like Glencore, Nyrstar Teck and MMG. For investors interested in more leverage (the kind offered by the juniors) there are only a handful of names and even fewer worth your money.

Trevali has been the ‘go to’ name in the space given their project portfolio and pipeline. They have a recently completed mine in Peru and development projects in Canada. Shares are up over 30% in 2014 as investors piled into the name to gain zinc exposure.

There are a number of other smaller cap companies at varying stages of exploration and development. Most of them face significant challenges, whether it’s metallurgy, permitting, CAPEX or any other mix of issues surrounding mining projects.

Given that backdrop, InZinc Mining (IZN.TSXV) has the opportunity to become the preeminent junior zinc developer in the sector. Its April 2014 PEA suggests that the company holds one of the most economically robust undeveloped zinc projects in the world; West Desert.

The project looks capable of producing nearly 50,000 tonnes of zinc per year, making it an attractive target for zinc producers looking for solid production growth from a safe mining jurisdiction. Furthermore, the project has significant by-products including magnetite and a rare critical metal known as indium which adds significantly to the optionality of the project.

Zinc: A Supply Story

For years, zinc proponents have been ‘calling’ a deficit in the zinc market, citing future mine closures and steadily increasing demand. Although those arguments (tightening supply and growing demand) are sound for an increase in any commodity price, the supply-side shortage took longer to materialize than some people expected with producers willing to completely exhaust their mines even if the tail end production was bleeding cash.

Source: CEO.ca, ILZRO

Now those mine closures causing supply-side strain are actually happening and the market is beginning to react to it. In fact, Glencore believes we will see a 260-270,000 tonne deficit in zinc concentrate in 2014. As a result, the price of zinc jumped 20% over the past year.

Because the demand side of zinc is relatively predictable (between 3 to 4% annual global growth), the price is supply-driven and as a result, major mine shutdowns play a big part in the zinc plot.

The third largest operating zinc mine, Century, is expected to stop mining operations in mid-2015 due to the ore body being completely depleted (not due to uneconomic metal prices). That removes approximately 500,000 tonnes of annual production from the market or roughly 3.5% (annual zinc market ~ 13 million tonnes per annum).

Glencore’s Brunswick and Perseverance mines in eastern Canada closed last year after exhausting their respective ore bodies. Combined, these two closures removed roughly 355,000 tonnes of production annually. Additionally, Vedanta’s Lisheen and Skorpion mines (Ireland and Namibia, respectively) are expected to shut by 2016, removing another 325,000 tonnes per annum.

With the planned closures and reductions at the world’s largest zinc operations, new mines simply can’t make up the difference. MMG’s Dugald River project, a 200,000 tonne per year development project, has been delayed while Glencore’s new Perkoa mine in Burkina Faso is adding only 80,000 tonnes annually. There are a number of expansions of existing operations which are expected to add roughly 350,000 tonnes in total.

Over the next 5 years, Glencore estimates that the market will need 3 million tonnes of zinc concentrate to meet demand while they expect non-Chinese mine production to add a maximum of 650,000 tonnes over that period.

So clearly, the market would need big production out of China, something that doesn’t appear likely given that over the past decade, mine production there has declined by 225,000 tonnes per year (the same as roughly one of the largest zinc mines in the world closing each year). Assuming China does increase mine supply by 220,000 tonnes per year, Glencore believes the next 5 years will see a global deficit of between 1 and 1.5 million tonnes of concentrates.

Zinc inventories are expected to drain quickly as the production deficit grows.

Glencore expects this to hit an inflection point by mid-2016 when inventories drop below the 3 weeks consumption threshold. Historically, zinc prices rise many months leading up to this inflection point.

West Desert

InZinc’s West Desert project is located in probably the most underrated mining jurisdiction in North America; Utah.

Western Utah, where the West Desert project is located, has a rich endowment of necessary mining infrastructure. The project itself has all-weather road access, on-site grid power, access to natural gas pipelines and is just 90 kilometres from two transcontinental rail lines. It is also roughly 125 kilometres from the massive, century-old Bingham Canyon copper mine.

West Desert project is located in mining friendly Utah (Source: InZinc Mining)

Utah isn’t generally thought of as a world-class mining jurisdiction, but it truly is. For example, the state recently approved Potash Ridge’s Large Mining Permit for their open-pit Blawn Mountain mine located in the southwest part of the State. The permit was granted within seven months of filing the application. It's tough to think of another jurisdiction in the world, let alone the US in which that would occur.

West Desert was previously the flagship asset of EuroZinc Mining until they transformed themselves into a producer by buying Neves Corvo, a major operating base metal mine in Portugal, and were subsequently acquired by the Lundin Group in 2006. Zinc prices were low at the time and InZinc (then Lithic Resources) was able to acquire West Desert (then named Crypto) from EuroZinc for next to nothing (US$ 25,000, 1.5 million shares and a 1.5% NSR royalty).

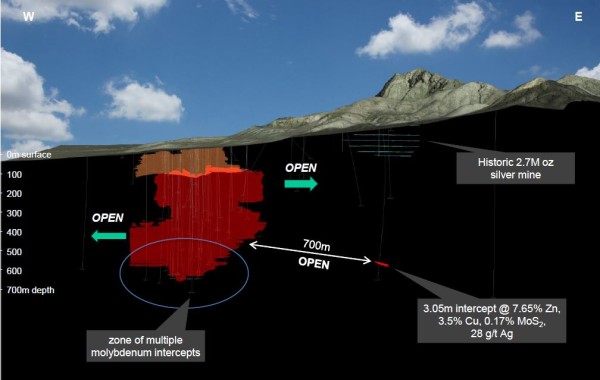

The project hosts a large underground resource of 13 million tonnes at 6.22% zinc equivalent (2.16% zinc, 0.23% copper and 48% magnetite), containing 691 million pounds of zinc, 65 million pounds of copper and 6.2 million tonnes of magnetite in the indicated category.

West Desert has a much larger inferred resource of 46 million tonnes at 5.57% zinc equivalent (1.76% zinc, 0.22% copper and 48% magnetite), containing 1.78 billion pounds of zinc, 224 million pounds of copper and 22 million tonnes of magnetite.

The resource is open for expansion in at least three directions.

The West Desert deposit remains open to the east and west and at depth (Source: InZinc Mining)

In early 2014, InZinc published an updated PEA (using US$1/lb zinc, copper at US$3/lb, iron ore at US$105/t (62% Fe, CFR-Tianjin), gold at US$1,300/oz and silver at US$21/oz) which envisages an initial 5,000 tonnes per day (“tpd”) ramp accessed underground operation ramping up to 6,500 tpd by year 3 capable of producing 108 million pounds of zinc, 10 million pounds of copper, 1 million tonnes of magnetite, 7,600 ounces of gold, 77,000 ounce of silver and 38 tonnes of indium annually over a 14.8 year mine-life.

Metallurgy is key with these types of skarn deposits, but CEO Chris Staargaard believes they have that under control.

“It is extremely clean mineralization and we've shown that completely conventional flotation processing would result in excellent recoveries. There are no deleterious elements such as arsenic, selenium or mercury. This, along with high levels of indium associated with zinc and payable gold and silver associated with copper, suggests that the concentrates are likely to be premium products,” says Mr. Staargaard.

The PEA includes Inferred resources, which will need to be converted to Indicated before they can be included in the company’s pre-feasibility or feasibility study.

The PEA also includes a substantial magnetite (iron ore concentrate) component which not only boosts revenues but also reduces costs.

In previous studies the magnetite was not viewed as part of the project’s economics but recent metallurgical work showed that it could be cheaply and efficiently extracted. As a result, 50% of the material that was previously deemed “tailings” (or expensive waste) was turned into 25% of the project’s forecast life-of-mine revenues.

Relative Valuation

With the polymetallic nature of the deposit and resultant byproduct credits, C1 cash costs are estimated at negative US$0.04 per pound of zinc while C3 costs are estimated at just US$0.50 per pound. To put that in perspective, the C1 cash costs for the West Desert project put it in the lowest 5% of global production (source: Brook Hunt/Wood Mackenzie).

Operating costs at West Desert are expected to be in the lowest quartile (Source: InZinc Mining)

Thanks to its infrastructure-rich location and standard mining/processing, the project CAPEX is also very manageable. Initial capital is estimated at US$ 247 million which is expected to be paid back within 3.7 years.

InZinc’s West Desert is the most attractive project in its peer group with a 23% after-tax IRR at long-term metal prices. The project also has significant optionality.

An important way to value junior explorers/developers is by relative valuation, that is, not only assigning value based on fundamentals, but also on what the market is currently assigning as value to comparable companies.

Although the company has one of the most advanced and economic development-stage projects in the Canadian equity markets, InZinc still trades at a deep discount to its peers and the peer group average. Below is a comparison of the Canadian publically-listed peer group:

Source: Company Reports, CEO.ca

With the credits in the concentrates, early-stage streaming is a possibility. You could also see private equity or a strategic get involved given the lack of available zinc projects and the high-quality and low risk nature of West Desert. Additionally, with the large magnetite component, an offtake financing arrangement could help advance the project as well.

Mr. Staargaard says that “with all of the significant mine closures over the next few years, the prospects for the zinc market have never looked better in my career.”

The company’s next step will be to do more drilling to continue expanding the deposit, upgrade the resource category and fine tune the CAPEX numbers as part of a pre-feasibility study. Permitting will be an ongoing process as well as the project is advanced.

The company raised just over $1 million (at double the current share price in September of last year) which has enabled them to refine drill targets. They will need to raise more capital to drill this year, but given the piquing interest in zinc plays, I would expect the company to be able to raise the necessary capital (~$2 million).

Given the lack of small-to-mid cap zinc plays, many analysts are watching InZinc, including those from Vancouver-based Haywood Securities, who believe the project will be able to garner attention from financiers and larger zinc producers.

The Team

Mr. Staargaard has financing help in at least two of his board members; Kerry Curtis (Chairman) and Wayne Hubert (Director). Mr. Curtis was the CEO of Cumberland Resources where he helped develop the Meadowbank gold project which he sold to Agnico-Eagle in 2007 for $730 million. Mr. Hubert was the CEO of Andean Resources which he led over a 4 year period where he grew the company’s resources from 800,000 ounces of gold to over 5 million and a market cap of $70 million to the $3.5 billion Goldcorp paid to acquire it.

As far as financing capabilities go, the board has been able to raise development dollars in the past and even though it is a challenging market, the West Desert project is one that will likely attract many sources of capital.

Management and the board own just over 17% of the company on a fully-diluted basis and institutions own another 15% (undiluted). The largest of these is the renowned mining fund, Geologic Resource Partners run by George Ireland.

Setting up for the Crunch

With zinc fundamentals coming to a head in the next 12 to 24 months, zinc equities are sure to benefit from the supply crunch. With such a small number of junior zinc stories (Canadian Zinc, Canada Zinc Metals, Zazu and Silver Bull to name a few), companies with the most advanced and de-risked projects will be the ones getting the first attention.

West Desert is an example of this, with some of the best projected economics in the peer group and a share price that reflects the current market environment and not the true value of the asset.

“We have been with this project for a long time. We know how hard it is to find a good project, regardless of the commodity,” the 35-year veteran, Mr. Staargaard says.

“If you find a good one, you hang on to it because eventually the market will come to you and it now looks as if zinc is going to be doing just that.”

If InZinc is able to even just catch up to the peer group average valuation, the stock could jump 5x.

To find out more about InZinc Mining Ltd. (TSX VENTURE:IZN) visit the Company’s website at www.inzincmining.com.

Disclaimer

The information contained in this article is for informational purposes only and may contain errors. The author owns shares of InZinc Mining Ltd.. The article is not intended to provide legal, accounting, tax, investment, financial or other advice to you, and you should not rely upon the information to provide any such advice. This article is not to be construed as a form of promotion, an offer to sell securities or as a solicitation to purchase our securities. This article has been produced as a source of general information only and opinion.

Cautionary Note Regarding Forward-Looking Statements

This article contains forward-looking statements and forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable Canadian and US securities legislation. All statements, other than statements of historical fact, included herein including, without limitation, statements regarding the Company’s next shareholder meeting. Although the Company believes that such statements are reasonable, it can give no assurance that such expectations will prove to be correct. Forward-looking statements are typically identified by words such as: believe, expect, anticipate, intend, estimate, postulate and similar expressions, or are those, which, by their nature, refer to future events. The Company cautions investors that any forward-looking statements by the Company are not guarantees of future results, performance, or actions and that actual results and actions may differ materially from those in forward-looking statements as a result of various factors, including, but not limited to, those risks and uncertainties disclosed in the Company’s Management Discussion and Analysis for the year ended December 31, 2013 filed with certain securities commissions in Canada and other information released by the Company and filed with the appropriate regulatory agencies. All of the Company's Canadian public disclosure filings may be accessed via www.sedar.com and readers are urged to review these materials, including the technical reports filed with respect to the Company's mineral properties.

A John Kaiser pick, I think.