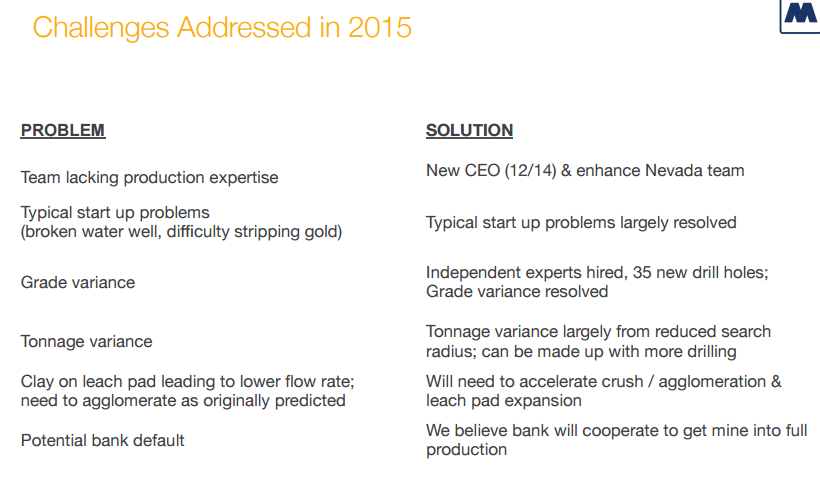

Midway challenges in 2015. (Image: Midway Gold)

A few interesting mining news releases this morning. Here are my top stories of the day with additional comments provided.

Midway Gold (MDW:TSX) - Midway Gold is out with an updated resources estimate at the newly producing Pan mine in Nevada. Midway has just started initial production at the mine and ~4300 ounces have been produced so far. It became clear that early on the previously modelled resource estimate was incorrect.

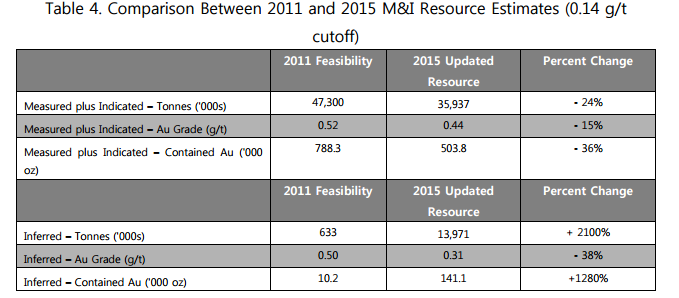

The new resource estimate at 0.27 g/t cut off models 443,300 ounces (Measured+Indicated) at a grade of 0.53 g/t gold. As well as an additional small inferred resource of 88,400 ounces of 0.53 g/t.

Note: The 2015 Measured, Indicated and Inferred resource was constrained within a $1,500 Lerchs-Grossman Pit shell. The base case estimate applies a cutoff grade of 0.14 g/t is based on the current operating costs, the 2011 Feasibility Study recoveries, and a $1,200 gold price.

Bill Zisch, Midway’s President & CEO commented, “Overcoming our startup challenges is the path to improving shareholder value as we are now a producing mine in Nevada. Completing the update of the resource at Pan provides us with a foundation for maximizing the performance of the Pan Mine and confirms the grade of the deposit. We are in the process of developing the optimal mine plan for Pan and initiating a drill program to expand the ore body. Our planned exploration activities include expansion drilling in the North and South extensions of the South Pan Pit where surface geologic mapping and sampling have demonstrated surface gold mineralization that has not yet been drill tested. We also plan to complete infill drilling in the Deep Wendy Zone. The updated model has been through extensive quality reviews as well as a comparison with production results and we are confident that it provides a good estimate of the deposit’s resources.”

The question is how does the updated resource compare to the the 2011 version? The answer is not great as shown in the table below.

The resource is 36% smaller. Not sure how the engineering firm Gustavson Associates could be so far off? More details will be available when Midway files the technical report on Sedar in 45 days.

An estimated 36,000 ounces are currently under heap leach at the Pan Mine.

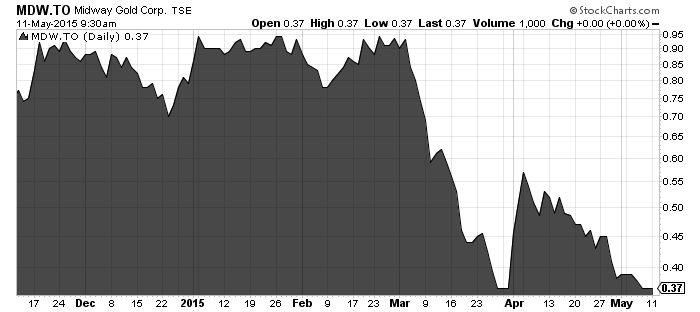

All in all bad news for Midway shareholders but it could already be baked into the share price.

A frustrating 6 month chart for Midway shareholders as production delays, grade issues, financial issues, and a drop in the gold price have all factored into a declining share price.

I continue to hold Midway shares.

Financial results are due out this month so we should be hearing more from Midway shortly.

Read: Midway Gold Updates Pan Modeling

Related: Why I have been buying this gold penny stock

Crocodile Gold - (CRK:TSX) - Crocodile Gold has agreed to merge wit Newmarket Gold (NGN:TSXV) to create a new gold industry consolidator. The combination will create a strong gold company with an experienced management group.

The deal:

- Each Newmarket shareholder will receive one NewCo common share for each Newmarket common share held;

- Each Crocodile Gold shareholder will have the option to elect to receive consideration per Crocodile Gold common share of (i) 1.228 NewCo shares, (ii) 37 Canadian cents in cash, or (iii) a combination thereof subject to a maximum aggregate cash consideration of $20-million (Canadian). Assuming full proration, shareholders of Crocodile Gold will receive 1.088 NewCo shares and 4.2 Canadian cents in cash for each Crocodile Gold share held.

The market likes the news sending CRK shares ~13% higher in early trading to 31 cents still below the 37 cent offer though.

Douglas Forster, president and chief executive officer of Newmarket, stated: "The combination of Newmarket and Crocodile Gold is designed to create a strong platform for future growth and consolidation in the gold sector. This transaction recognizes the deep value of Crocodile Gold's Australian operations that produce more than 200,000 ounces of gold annually, and the excellent work of Rodney Lamond and his team having turned Crocodile Gold's diverse operating mines into strong, stable cash flow generators. This transaction is a significant step in Newmarket's goal to deliver both immediate and long-term value to shareholders through the disciplined acquisition of quality gold assets in politically stable jurisdictions worldwide. Newmarket founder's and management's direct participation via the concurrent private placement financing demonstrates our commitment to aligning management's goals with those of our shareholders and to creating significant shareholder wealth."

Rodney Lamond, president and chief executive officer of Crocodile Gold, stated: "The board and management of Crocodile Gold fully support the planned combination between our two companies. NewCo will be well managed by a board of directors and senior executive management team that have an excellent track record and history of successfully growing large portfolios of mines and projects. NewCo provides an opportunity for Crocodile Gold's shareholders to participate in the long-term value and advancement of our existing assets while growing through future acquisitions. We believe this business combination will begin to benefit shareholders of both companies immediately."

A good deal that will have the NewCo with production of ~200,000 ounces that is generating free cash flow and $40 million on the balance sheet.

The transaction is expected to close in the third quarter.

Newmarket has been looking to do a deal in the mining space for a good 18 months before pulling the trigger on today's news.

I was on the Crocodile Gold story early in April for CEO.ca readers/chatters.

Read: Newmarket Gold and Crocodile Gold Merge to Establish a New Platform for Gold Asset Consolidation

Related: A look at Crocodile Gold, Eastern Platinum, and Endeavour Mining news or NGN - Newmaket Gold CEO Doug Forster Reveals Roll-Up Strategy

Constantine Metal - (CEM:TSX) - Constantine has reported a 97% increase in resource expansion for the the Palmer copper-zinc-silver-gold project, located in southeast Alaska. The updated resource involves almost double the drill holes and has been successful in doubling the size of the deposit. The Palmer joint venture project owned 51% by Constantine and 49% Dowa Metals and Mining a Japanese partner.

Garfield MacVeigh, president and chief executive officer of the company, stated: "The resource estimate significantly increases the size of the deposit, highlighting the tremendous success of recent drill campaigns and the growing potential of the project. It is open to expansion in most areas, with the thickest part of the deposit located at the current down-dip limit of the South Wall zone, where mineral zoning and geophysics support potential for a high-grade copper core within a more extensive area of zinc-copper-barite mineralization. A $5-million (U.S.) exploration budget is in place for 2015 to target extensions to the deposit, which are readily accessible by surface drilling."

The new resource estimate is:

Cut-off Grade NSR Cu Zn Au Ag CuEq ZnEq U.S. $ Tonnes (%) (%) (g/t) (g/t) (%) (%) 60 9,133,000 1.30 5.00 0.30 30.2 3.03 11.83 75 8,125,000 1.41 5.25 0.32 31.7 3.23 12.61 95 7,072,000 1.51 5.53 0.34 33.7 3.43 13.39

It appears the deposit has potential to get bigger and a $5 million dollar drill program will include step out drilling.

Insider ownership is ~27% which is a very positive sign.

I will be watching the CEM drill results this summer to see if the deposit continues to grow.

Related: Video - Darwin Green, VP of Exploration, Constantine Metal Resources (CEM.TSXV)

Discuss in CEO Live – What is catching your eye today?

This is not investment advice. All facts are to be checked and verified by reader. As always please do your own due diligence. Author owns a position in Midway Gold and is therefore biased.