A look at some of my favourite news releases out this morning with some brief comments on each.

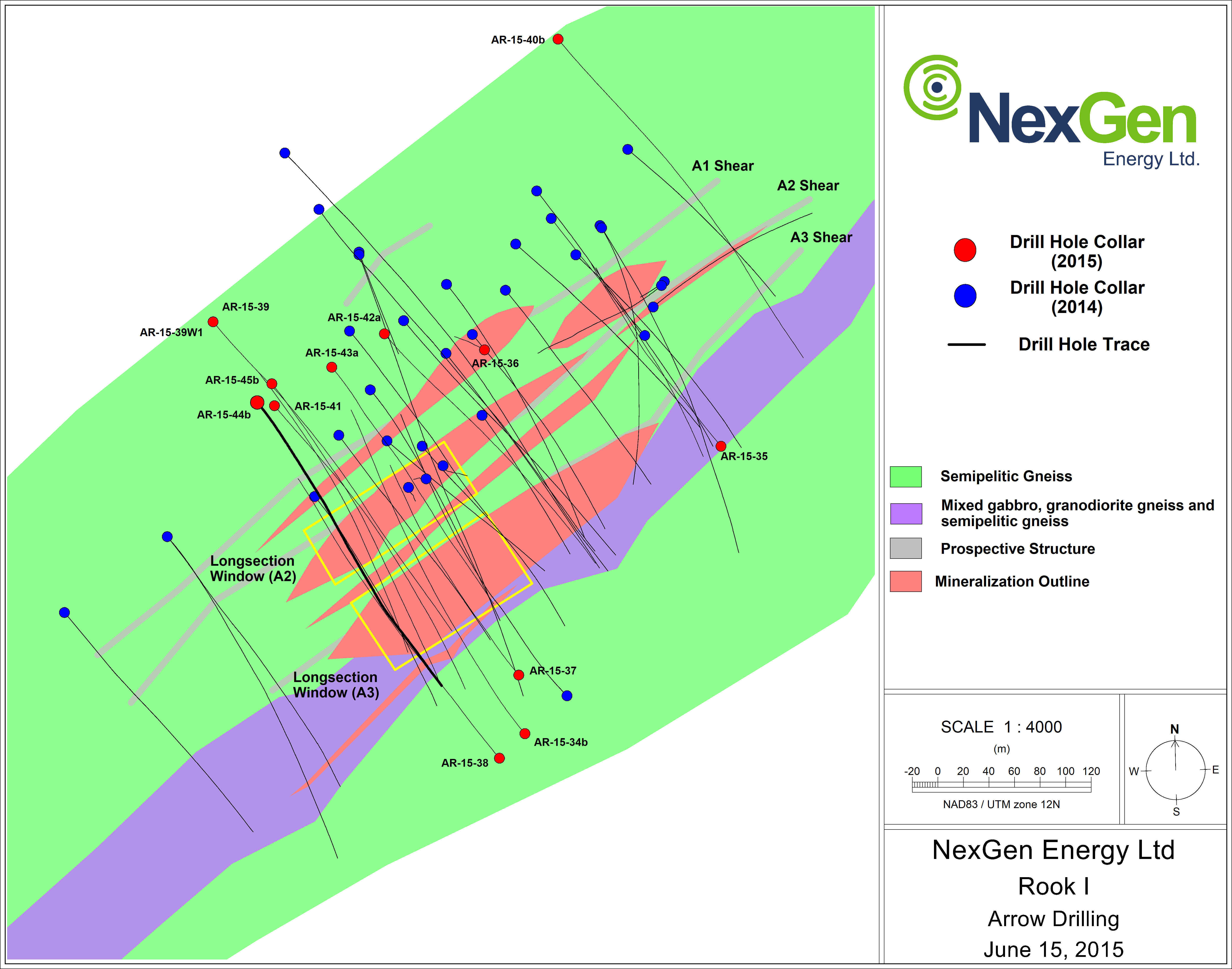

NexGen Energy - (NXE:TSXV) - A huge drill hole out of NexGen Energy this morning as hole AR-15-44b has intersected 68.5 m of 9.56% U3O8 at the Rook 1 project in Saskatchewan. Rook 1 is located in the best place in the world for uranium exploration the Athabasca region. NexGen continues to be one of the top uranium exploration names in the space and the Rook 1 project is rapidly growing.

Highlights:

- AR-15-44b showcases Arrow as a world-class discovery resulting in a total composite grade thickness (“GT”) of 853.55;

- 56.5 m at 11.55% U3O8 (499.5 to 556.0 m) including 20.0 m at 20.68% U3O8 (499.5 to 519.5 m) and 1.0 m at 70.00% U3O8 (503.0 to 504.0 m);

- The most continually mineralized intersection at the Arrow zone to date with a GT of 654.78 ranking it as one of the top drill holes ever in uranium exploration;

- Located on the current south western edge of the high grade core zones of A2 and A3 shears . Summer drilling to step out further to the untested south west;

- The Arrow zone is currently 515m by 215m with the vertical extent of mineralization commencing from 100m and extending down to 920m, and is open in all directions;

- Two of five rigs of the 25,000m $9 Million summer drill program commenced June 8, 2015;

- The Company is well financed with working capital of $30 Million

Garrett Ainsworth, NexGen's Vice-President, Exploration and Development, commented "This world-class result from AR-15-44b will add substantial size to the rapidly developing Arrow zone. When increasing the internal dilution from 2.0 m to 4.5 m, this drill hole returns a total composite interval of 168.5 m at 5.00% U3O8 (455.5 to 624.0 m) representing an estimated true thickness of 43.6 m with only 1.2 m of estimated true thickness internal dilution. The summer 2015 drill program is now underway, and the technical team is excited to continue delineating and expanding the high grade Arrow zone, together with testing the high priority regional geophysical targets.

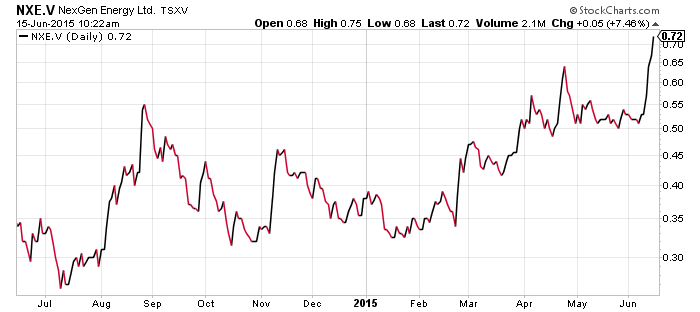

NexGen Energy is one of the bright spots on the TSX Venture this year doubling in share price and is printing an all time high this morning.

The stock is one of the most popular stocks on CEO Live and all comments can be found here.

Many investors believe NXE stock still has quite the room to run to close the valuation gap with Fission Energy (FCU:TSX).

NXE market cap ~$142 million.

FCU market cap ~$421 million.

Fission is further along the development stage with resource estimate out and a PEA expected later this summer. NexGen plans on releasing a 43-101 resource estimate later this year.

Plenty of news flow is expected in the summer months as a 25,000m summer drill program is under way.

For those investors looking for a little more 'juice' NexGen has a trading warrant NXE.wt.

Read: NexGen Intersects 56.5m at 11.55% U3O8 Including 20.0m at 20.68% U3O8 in Hole AR-15-44b

Related: NexGen Energy CEO Leigh Curyer: “Arrow is quickly becoming a significant discovery”

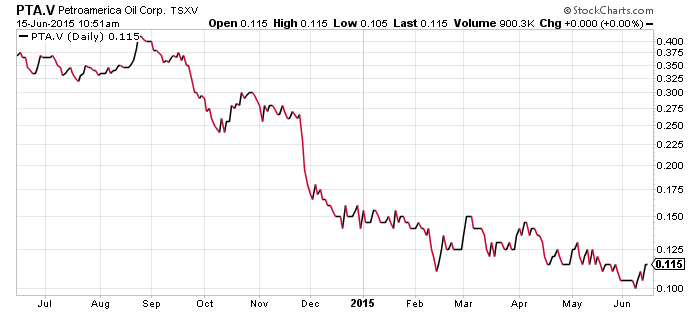

Petroamerica Oil - (PTA:TSXV) - Petroamerica has made an share offer to acquire Colombian oil junior Petronova (PNA:TSXV). The offer represents a 15% premium for Petronova shareholders and is expected to close at the end of July.

Key attributes of PetroNova

- PetroNova operates and holds a 75-per-cent and 40-per-cent working interest (WI) in the PUT-2 and Tinigua blocks in the Caguan-Putumayo basin of Colombia and holds a 20-per-cent non-operated WI in both the CPO-7 and CPO-13 blocks in the Eastern Llanos basin in Colombia.

- There is significant prospective resource upside potential, especially on the Tinigua block.

- Proved and probable (2P) WI reserves (before royalty) as at Dec. 31, 2014, are 6.3 million barrels (mmbbl) (after royalty 3.5 mmbbl) with before-tax net present value (discounted at 10 per cent) of $67.2-million.

- All four of PetroNova's blocks have environmental licences in place.

- PetroNova has exposure to 1.3 million gross acres in Colombia with an extensive portfolio of drill-ready prospects.

- PetroNova farmed out a 50-per-cent working interest in the Tinigua block to a wholly owned subsidiary of Pacific Rubiales for $12.5-million in back costs and Pacific Rubiales will carry the cost of drilling, completing and testing of up to two wells for up to $19-million.

- Pacific Rubiales will also finance the cost of two additional wells for $14-million, to be paid back from PetroNova future production from these wells.

- PetroNova holds a 75-per-cent-operated WI in the PUT-2 block (Petroamerica holding the other 25-per-cent working interest) which holds multiple N-sand prospects and leads.

- The CPO-13 block is adjacent to the prolific Rubiales and Quifa heavy oil fields and the heavy oil trend has been confirmed to extend onto PetroNova's block.

- PetroNova's WI production during the month of May, 2015, averaged 304 barrels (bbl) per day (bbl/d) of oil from two discoveries in the Llanos basin.

- PetroNova assets have minimal near-term commitments and are unencumbered.

"This acquisition ticks a number of boxes for Petroamerica, delivering significant strategic, financial and operational benefits, as well as medium- to long-term growth potential for both the company and shareholders alike. PetroNova's portfolio is highly complementary to our existing asset base bringing reserves, near-term reserve growth potential, operatorship (of two blocks) and significant exploration upside including one of the largest undrilled foothills structures covered by 3-D seismic in Colombia. It further consolidates our land position in the prolific N-sand play in the Putumayo basin with a 100-per-cent-operated WI position in the PUT-2 block, and provides exposure to a world-class medium to heavy oil play in the Eastern Llanos basin, with two blocks abutting the significant oil fields of Rubiales, Quifa and Caracara. PetroNova's blocks come with minimal near-term commitments and given that Petroamerica is currently debt free, we should find ourselves better positioned to leverage these additional reserves in a debt market that continues to improve," commented Ralph Gillcrist, president and chief executive officer of Petroamerica.

PTA stock has suffered due to low oil prices and operational issues. The company has one advantage of being debt free.

This is the second transaction PTA has made in the last year following the acquisition of Suroco. The business is being set up for a turn around in oil prices.

Related: Have Patience: Petroamerica Oil CEO

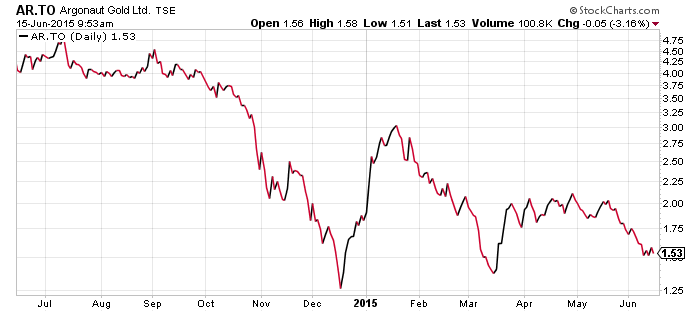

Argonaut Gold - (AR:TSX) - Argonaut Gold is out with drill results from the Magino project in Ontario. The drilling was successful in extending the mineralization 250 metres further east on the Richmont zone.

Drilling was highlighted by hole MA15-439 intersecting 98.8 m of 1.69 g/t.

Argonaut acquired the Richmont zone from Richmont Mines (RIC:TSX) in a 2013 deal. The Magino project is adjacent to the Island Gold Mine of Richmont. Although the projects are in close proximity they are on two separate geological structures. Richmont is in production and high grade material while Argonaut is looking at a open pit scenario (low grade).

Peter Dougherty, President and CEO of Argonaut Gold stated: "I am pleased with the progress the Company is making at Magino. This project hits on so many of the key evaluation metrics we look for in a project. It is a multi-million ounce deposit that greatly benefits from the advantages that come with being located in one of the top mining countries of the world. These drill results show both extended mineralization and higher grades. As we continue to test the extensions of the deposit, we are excited about the potential to increase the resource and value of this project.”

Magino was purchased in the last gold bull market for $341 million when Argonaut purchased Prodigy Gold. To put it into perspective Argonaut's market cap is only $240 million this morning.

Magino has resources of 6.25 million ounces and looks like it could get bigger with today's news. At $1250 gold a feasibility study on 40% of the resource shows an IRR of 21% with a CAPEX of $364 million.

Related: The hottest gold stock on the planet

This is not investment advice. All facts are to be checked and verified by reader. As always please do your own due diligence.