Bloomberg

"When they raid the house of ill repute, they arrest everyone including the piano player"

That colourful sentence could certainly be used to describe the current rout in commodity markets, however, should the entire basket be thrown together, i.e. bulks, precious metals, agriculture and the PhD of the economy, copper? Or, is there in fact a “piano player” in the mix?

Goldman Sachs (GS) released a powerful update to their clients on July 22nd painting a very negative picture for copper prices. GS research is changing course on copper from a previously bullish stance, suggesting that due to slowing growth in China, by far the world's largest user of most commodities, and a coming copper supply glut, the price of copper is doomed to stay in the ~$2.00/lb range (recently $2.90/lb and one year ago $3.20/lb) all the way to 2020. There is more than one side to this coin, in fact, one should review the various pillars that underpin this bold call.

The prognostication GS has made on copper prices is certainly based on facts and logic supported by their view of supply and demand fundamentals. What is unmistakeable, is that their opinion has significant weight for many global investors, especially the swing traders who often make big differences in turbulent markets. Value investor Ben Graham once said (paraphrasing), "that in the short-term markets are like voting machines, whereas in the long-term they are weighing machines." I fully agree, and investors the world over have voted with the overwhelmingly bearish sentiment that has put commodities on a one-way trade downward, and perhaps quite rightfully so for the ones that have had an idiotic over-allocation of capital, namely the bulks, and the over-hypothecated precious metals. A strengthening US dollar, negative headlines in Europe, China’s ‘around 7% growth’, Asian stock markets collapsing, just to name a few of the macro problems plaguing global growth, and in-turn, commodities.

Is Copper the piano player in the commodity complex? It's all about the consumer, and that means the tightness between demand and supply.

Demand.

Copper, unlike other highly traded commodities, namely oil and gold, is not so hypothecated. The end user of copper is just that, a user, and not a speculator. True, there has been some 500,000 tonnes (maybe a bit more) of copper used as ‘money’, however, for the most part, almost all of the ~23 million tonnes of produced copper is consumed. Many of the major end users of copper are now in a very bearish to the short-term copper price - hand-to-mouth mode - and why shouldn’t they be? Just look at China's State Reserves Bureau (SRB), one of the biggest buyers of copper, who bought 400-700kt's during 2014. Copper prices have fallen by ~20% since, thus the SRB has paid $100's of millions more than they could today. So big buyers can wait - hand-to-mouth - and they do.

Consumers are not greedy in a falling price environment, it's quite the opposite. If material can be readily found and they are quite comfortable there should be no spike in the price, then why allocate precious capital? This will not change until bearish sentiment changes, or more importantly, until tighter supply and demand conditions return. The question then becomes, can a market shortfall for copper happen sooner than GS's 2020 time period, thus inducing end users to once again become greedy and start buying copper from the offer, other than hand-to-mouth consumption?

Of course what happens in China is important. This must be monitored and global investors and consumers will do just that, but... there are other factors.

Oil is energy, and energy without fossil fuels actually means electricity and electricity demands copper. Traditionally, oil and energy have lead other commodities through most of the big up and down price swings - just look at any 40 or 50 year chart that correlates, oil to gold and/or copper. If there are going to be winners and losers in the future of energy, then oil and coal, to some respect, are the losers, and copper will overwhelmingly be the winner as it takes between three and five times more copper per megawatt of utility, the cleaner and greener we create, utilize and transfer energy. I will suggest the future is now, and that humanity has an incalculable number of ways that we are accelerating the subliminal ways we are using more and more copper. Unless fully appreciated, these dramatic changes could never fit on the pages of any report, let alone the GS document on copper that is perhaps missing all the utility copper plays from an electrifying India all the way to Elon Musk's Giga Factory.

Supply.

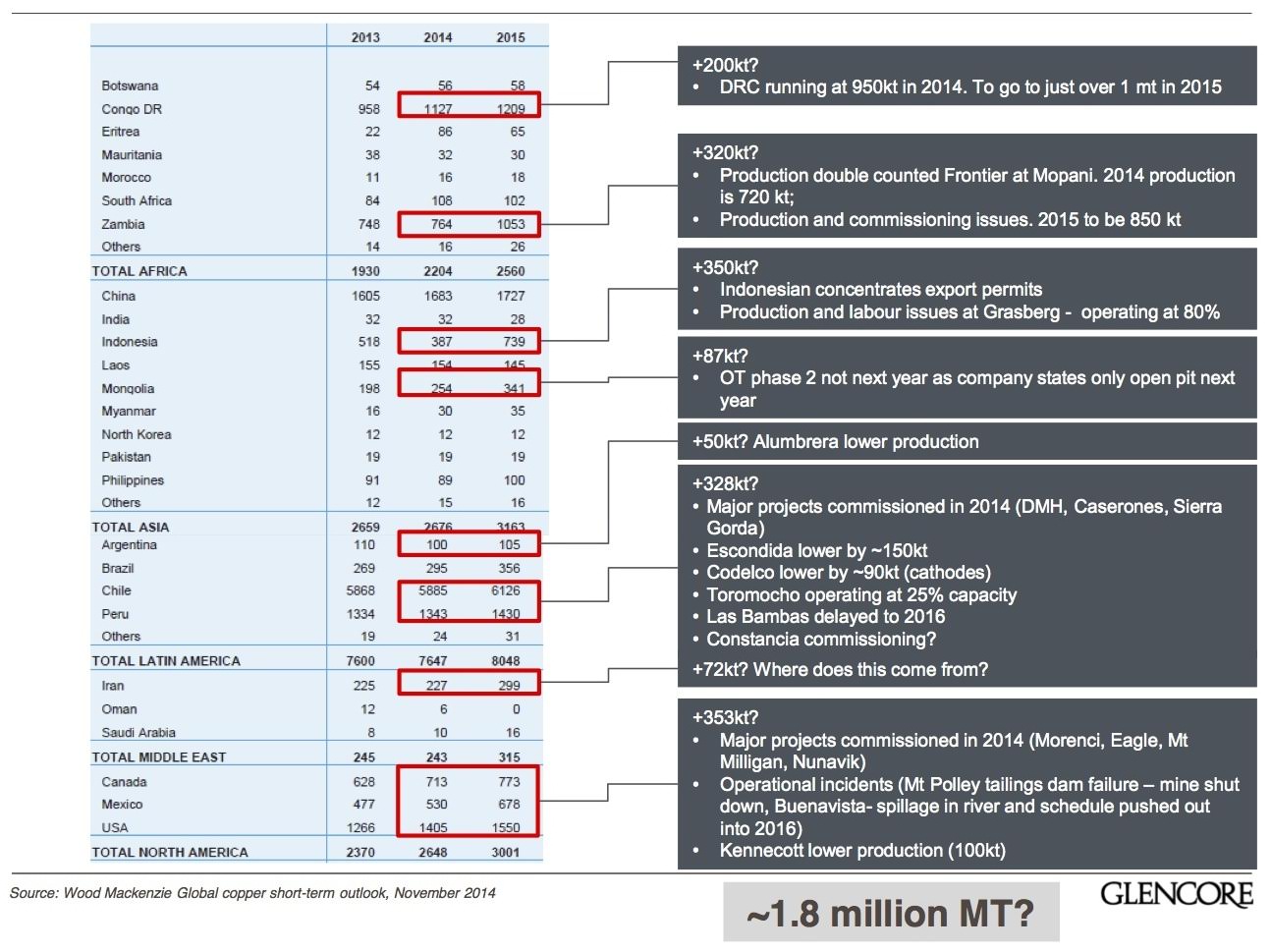

According to their report, GS believes that the top 15 contributors to new copper supply will offer some 1.7 million tonnes of net new copper. On the other side of the coin there is Glencore, one of the biggest producers of copper in the world, and the largest trader of copper, some 50% of traffic, who would seemingly disagree with some of GS's production forecasts. So who is to be considered more accurate, analysts, or those that are on the pulse of most of the copper operations around the world? Telis Mistakidis, the head of Glencore's copper division, has suggested that analysts should take a closer look at supply side guidance. In the video archive of their December 2014 Investor Day presentation, he gives a country by country run-down of all the likely new production that should enter the market in the coming years. As he then stated, "we don't see a supply glut."

GLENCORE'S COUNTRY BY COUNTRY AUDIT OF COPPER PRODUCTION GUIDANCE

GS is quite correct in stating that there are only a handful of companies that produce global copper. BHP, the world's largest integrated miner, suggests the inducement price for ~70% of future copper projects is $3.50/lb, and nothing works at sub $2.50/lb. Just recently they gave guidance to the market that their 2016 copper production will fall by 12%. The largest producer of copper, Chile's CODELCO, is telling the market they could cease to be a copper producer past 2030 without some $25 billion of expansion capital. The achilles heel of copper production is falling grade, and as any miner will tell you, when you are mining 30 or 40 million tonnes per year, in 400 tonne trucks, it's a big big deal when grade falls by 50%.

What about selling concentrate with big penalties like Toromocho, who the GS report see's no problem in placing 240kt's of reliable future product on the market. Sentinel? Katanga? Africa's copperbelt is seriously power constrained fyi. Chile is having to reconsider social program promises made during the $4.00/lb copper days to the realities of today. Peru?

So who will be more correct? As has been demonstrated in the past, not everyone can be right. I recall in early 2009 when two respected analysts had diametrically opposed views of my then favourite investment, Quadra Mining (early 2009 trading at ~$2.50 per share). One analyst saw weak copper prices into the distant future and as such he placed a $2.50 price target on Quadra. The other analyst, saw stronger copper prices going into 2010 and 2011 and he placed a $21.00 price target. One year later Quadra was $18.00 per share. How could two well respected professionals have such different views?

For now prices for most commodities are falling, and why should that stop. But let us not forget:

"When they raid the house of ill repute, they arrest everyone including the piano player"

Gianni Kovacevic is a co-founder and the Executive Chairman of Copperbank Resources Corp (CSE:CBK). Learn more about Copperbank here.