An interesting chart on the silver cyle First Majestic has in the latest corporate presentation. (Image: First Majestic)

A look at news out this morning from First Majestic Silver and Fission Uranium with some additional comments added.

First Majestic Silver - (FR:TSX) - First Majestic Silver is out with second quarter financials. Net loss for the quarter came in at $2.6 million ($0.02 cents per share). Production for the quarter was 2.7 million ounces of silver or 3.8 million silver equivalent ounces.

Another silver company that posts a net loss during the quarter albeit a small one. Of note to investors is that the average realized price of silver for the quarter was $16.99.

Current price of silver this morning is $15.25 so it looks like Q3 FR will be posting another loss unless drastic operational improvements.

First Majestic did make an acquisition of SilverCrest Mines recently which I see as a positive move.

Second Quarter Highlights

- Generated revenues of $54.2 million

- Mine operating earnings amounted to $3.4 million

- Operating cash flows before movements in working capital and taxes of $16.4 million or $0.14 per share

- Total cash cost, net of by-product credits, was $8.74 per payable silver ounce

- All-in sustaining cost ("AISC") was $14.49 per payable silver ounce, a 20% reduction compared to $18.18 per ounce in second quarter of 2014

- Average realized selling price for silver was $16.99 per ounce, compared to the quarterly COMEX average silver price of $16.38 per ounce

- Cash and cash equivalents of $37.7 million held at the end of the quarter

Keith Neumeyer, President and CEO of First Majestic, stated: "Our all-in sustaining cash costs in the first half of 2015 came in at the low end of guidance at $14.18 per ounce, or a 23% reduction compared to $18.46 per ounce in the first half of 2014. Cost reductions at Del Toro have had a great impact on our bottom line with all-in sustaining costs falling to $7.13 per ounce in the first half of the year compared to $21.52 per ounce in the first half of 2014. Additional cost savings are anticipated in the second half of 2015 as we realize higher operational efficiencies at La Encantada due to its recent expansion to 3,000 tpd."

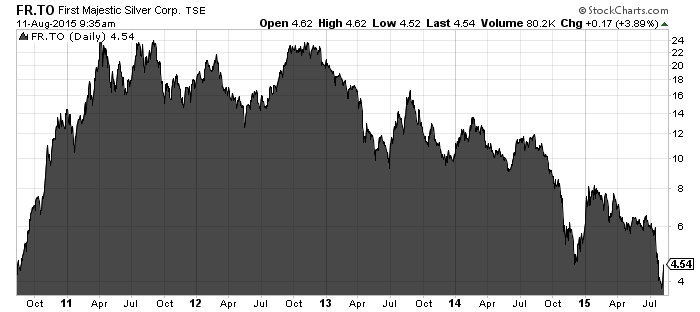

The 5 year chart of FR is a great example of the volatility in the mining business. From $4 to $24 all the way back to $4 in a few years.

A quick peek at the balance sheet as at June 30th shows $37.7 million in cash and cash equivalents and $73.25 million in current liabilities (yikes!).

With only a couple silver producer making a profit at the current silver price I would have to think it can't be long before we see mines shut down.

I learned from Rick Rule at the recent Sprott-Stansberry Symposium bull markets are created in two ways either from demand construction or supply destruction.

Read: 2nd Quarter Financial Statements - June 30, 2015

Related: Monday Morning News – First Majestic Silver, SilverCrest Mines, and Galantas Gold

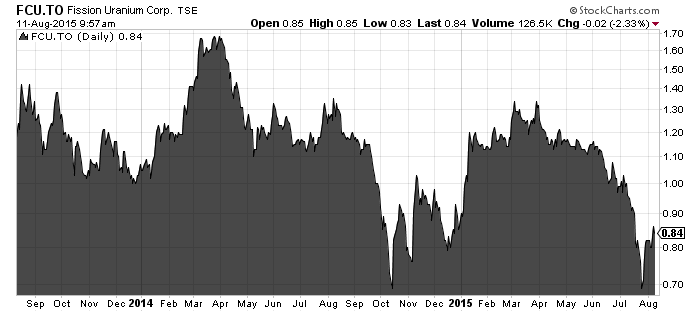

Fission Uranium - (FCU:TSX) - Shares of Fission continue to languish (last at 82 cents) after the announcement of the merger with Denison (DML:TSX). News out this morning included results for 10 holes of the 60 hole 20,000 metre summer program.

Fission continues to hit with all 10 holes intersecting mineralization and 6 measuring over 10,000 cps.

Drilling highlights include:

R600W zone:

- Expanded R600W zone an additional 15 m west (to line 675W) by high-grade hole PLS15-408 and a further 15 m east (to line 570W) with hole PLS15-404;

- R600W zone now extended to a strike length of 105 m.

R780E zone:

- Considerable high-grade mineralization encountered on line 1125E (hole PLS15-416).

Ross McElroy, president, chief operating officer and chief geologist for Fission, commented:

"We have now intercepted substantial high-grade mineralization on the far eastern side of the R780E zone (line 1125E), with the strongest mineralization to date in that area. In addition, the high-grade, shallow depth R600W zone has now reached 105 m in strike length and continues to show a rapid growth rate with a style of mineralization similar to that of the Triple R's R780E zone, over half a kilometre on strike to the east."

A two year chat of FCU shows the stock close to 2 year lows.

A major catalyst for the stock is upcoming with a PEA. At the Sprott-Stansberry conference FIS still had summer 2015 on the timeline for the PEA.

The deal between Fission and Denison is expected to occur in October. I would not be surprised to see another bid come in for Fission if the PEA results come in good.

Read: Fission Hits Broad High-Grade Mineralization at Eastern Edge of Triple R Deposit (Line 1125E)

Related: Video: Brent Cook and Ross McElroy discuss good Fission Uranium news, live from the PDAC

Thanks for reading.

This is not investment advice. All facts are to be checked and verified by reader. As always please do your own due diligence.