A look at the top mining press releases out this morning with some additional comments on each.

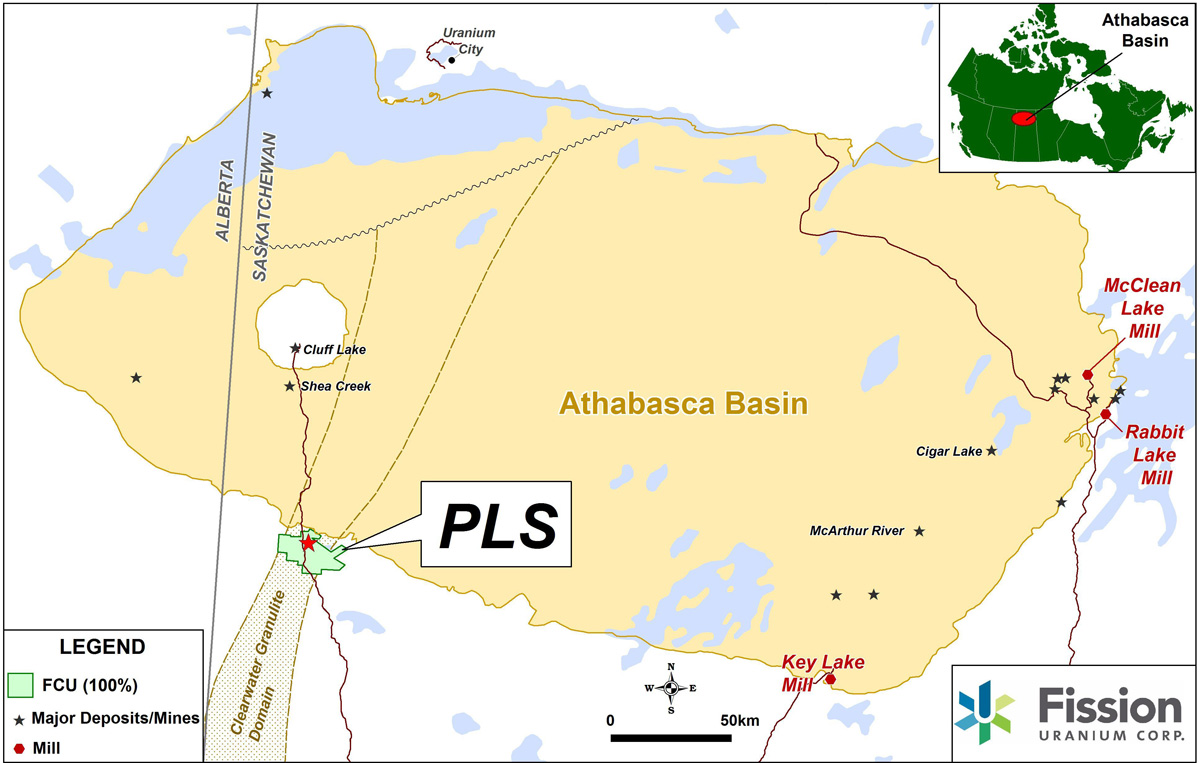

Fission Uranium - (FCU:TSX) - Fission is out with a PEA on the Triple R Deposit on the PLS property in the Athabasca Basin. The PEA was completed by RPA Inc.

The PEA does show an attractive post tax IRR of 34.2% and post tax NPV of $1.02 billion.

Investors should note that FCU uses a uranium price of $65.oo/lb for this study while the current spot price is $36.75/lb. Also the PEA includes inferred resources which are to speculative geologically to have economic considerations applied.

Highlights

- Base case pre-tax Net Present Value ("NPV") of $1.81 billion, post-tax NPV of $1.02 billion (10% discount rate)

- Mine life of 14 years producing an estimated 100.8 million pounds of yellowcake at a metallurgical recovery of 95%with 77.5 million pounds of U3O8 recovered in the first 6 years of production

- Average annual production of 7.2 million lbs U3O8 over the life of mine

- Base case pre-tax Net Cash Flow over the proposed mine life of $4.12 billion, post-tax Net Cash Flow of $2.53 billion

- Base case pre-tax Internal Rate of Return ("IRR") of 46.7%, post-tax IRR of 34.2%

- Pay back estimated at 1.4 years (pre-tax), pay back at 1.7 year (post-tax)

- Estimated initial capital costs ("CAPEX") of $1.1 billion

- Average operating costs ("OPEX") of US$14.02/lb U3O8 over the life of mine

(Base case using US$65/lb U3O8 and an exchange rate of US$0.85:C$1.00). All values in C$ unless otherwise noted.

Ross McElroy, President, COO, and Chief Geologist for Fission, commented,

"This PEA is an incredibly important milestone, and shows the viability of development and profitability of the unique, shallow, large and high-grade Triple R uranium deposit. The study confirms this unique deposit is a robust project with very strong economics. With anticipated operating costs of US$14.02/lb and a pre-tax IRR of 46.7%, we are looking at low cost production with a payback and highly profitable life of mine. It's also important to note that the recently discovered, high-grade R600W zone, which was not included in the PEA, has the potential to add a great deal to the bottom line as the Triple R continues to grow. Additionally, a mill at PLS has the potential to become a key centerpiece for the Western Athabasca Basin - with the potential to process ore from other high-grade projects in the region as they are taken into production."

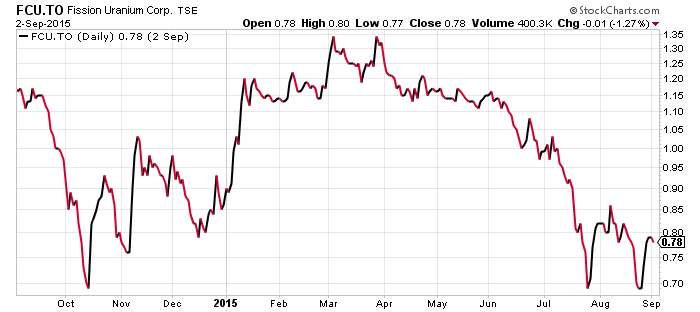

Fission share price has had quite the ride in 2015. The stock is trading near 52 week lows currently as the merger with Denison is pending shareholder approval expected in October.

This still gives time for a competing bid to develop if a majors interest is peaked by this PEA.

Cameco the bell weather stock for the uranium space also recently hit a 52 week low but has since rebounded a little bit.

The uranium market can not seem to gain any traction but fundamentals do look strong down the road.

Several members of CEO chat commented on the PEA and everything can be found in the $FCU room at http://chat.ceo.ca/fcu

Related: Denison and Fission Announce Transaction to Create Leading Diversified Uranium Company

Amarc Resources (AHR:TSXV) and Thompson Creek Metals (TCM:TSX) - Amarc has optioned the IKE project to Thompson Creek Metals. IKE is a copper-molybdenum-silver deposit with prospective targets yet to be drilled. Thompson Creek will earn into a 30% interest by spending $15 million over the next 4-5 years.

An additional 20% interest can be earned if TCM meets additional conditions which would include a feasibility study.

The agreement

- To earn 30% Thompson Creek must spend $15 milllion on the property before December 31st, 2019.

- $3 million is committed for this year.

- For each $5 million in expenditures TCM will incrementally earn 10% interest.

- Amarc will remain project operator.

- If stage 1 (30% interest) is fully exercised TCM can earn an additional 20% by meeting certain conditions for a total of 50% interest in the project.

- To earn the additional 20% TCM will within 120 days of completing stage 1 finance and complete a feasibility study.

- The feasibility study must be completed within a 2 year period but can be extended to 3 under certain circumstances.

Robert Dickinson, chairman of Amarc: "HDI companies have a long history of discovering and developing copper porphyry deposits in B.C. that have gone on to generate decades of wealth and opportunity for British Columbians. Thompson Creek's Mount Milligan mine northwest of Prince George, for example, is a copper-gold porphyry that our group drilled and discovered years ago. We're delighted that today, under Thompson Creek's committed leadership, it is generating high-value jobs and economic benefits for British Columbians, and we are excited to be joining forces with Thompson Creek at IKE, a property we believe has the potential to become a company maker in the years ahead."

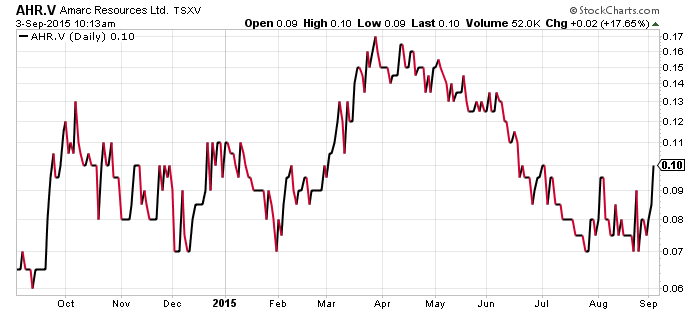

Amarc shares are up 1.5 cents (17.65%) to 10 cents this morning on volume of 62,000 shares traded (at press time) giving the company a market cap of ~$14 million.

The exciting news for shareholders is that $3 million is scheduled to be spent in 2015.

Crews are expected to be mobilized to the project soon and drilling will focus on the IKE porphyry system to determine the known deposit's full resource potential.

Amarc is currently permitted for up to 50 drill holes.

The $3 million dollar program is expected to provide steady news flow over the next several months. Investors will be eagerly waiting to see if AHR and TCM can find some higher grade mineralization as current drill holes are ~0.40 CuEq%.

Read: Amarc and Thompson Creek Partner to Advance the IKE Copper Porphyry Project

Related: Diane Nicolson's August message from the president or Dickinson’s Amarc drumbeating is working

Thanks for reading.

This is not investment advice. All facts are to be checked and verified by reader. As always please do your own due diligence.