Chow Tai Fook, Greater China's largest diamond retailer, Beijing. Source: Chow Tai Fook.

Given the current inclement state of the diamond industry, I thought it would be useful to take a few steps back and break the convoluted dynamics of the industry down into the simplest fundamental concept in economics: supply and demand.

Despite the fact that the diamond industry is heavily concentrated, and still possesses tones congruent with its relatively recently removed history of being a monopoly, end-consumer demand is still what ultimately drives the health of the industry longer-term. Supply dynamics play more of an intermittent role as the demand picture plays out over time.

DEMAND PICTURE

Within the last two weeks both ALROSA (RTS: ALRS) and De Beers have indicated that global demand jewelry demand is going to be -2%-to-flat in 2015.

With U.S. and Mainland China demand for diamond jewelry relatively stable in 2015, industry participants have indicated the weakness this year is primarily attributed to the Hong Kong and Macau segment of the Greater China market, with Hong Kong more specifically impacted by a reduction in mainland tourism due to a weaker yuan, and Macau impacted by continued government campaigns targeting corrupt luxury gift giving.

While a moderate net decrease in Chinese demand for diamond jewelry is expected this year, I think it is important to remember that demand is still relatively stable. What is more significant is the change in the rate of growth of demand, which is ebbing as the region transitions to a more of a consumer driven economy (which should eventually have a longer-term positive impact on discretionary luxury items like diamonds).

The underlying Chinese appetite and ability to purchase diamonds is by no means going away. In fact, the market is still so influential that the industry’s peripheral markets: Europe, the Middle East, Japan, and Australia are circumstantially being driven by Chinese tourism. Two weeks ago, Tiffany (NYSE: TIF) specifically attributed optimistic Q3 results in their Japanese market to an increase in Chinese tourist traffic.

SUPPLY OVERHANG

Demand for diamonds over the last year-and-a-half has not been great enough to keep up with the midstream segment’s (the cutters and manufactures) excessive speculation through expansion that began 5 years prior. The impact became exceedingly apparent in late 2014, and further exacerbated around the time the Chinese devaluated the yuan in August of this year.

According to De Beers this week, banks historically would finance 100% of their clients rough diamond purchases, but this year equivalent lending was to down to 60-70%. While the midstream segment has certainly felt squeezed by the rough/polished price spread and credit availability in recent quarters, it's unclear the extent that this has impacted the longer-term livelihood of the segment.

A diamond being cut. Source: De Beers

Some bankruptcies have been seen in the midstream segment, which is concerning, but none of the major players have been squeezed out of business. There really has not been a mass exodus, or even consolidation, in the midstream space, despite the alarming sentiment. So the question becomes, are conditions in the mid-stream segment not as bad as indicated, or is it just a matter of time before that segment of the industry really collapses?

The upstream segment's (the miners) response to market conditions was a bit lagged, but this year all of the major diamond producers cut supply available for sale, cut prices, or a combination of the two.

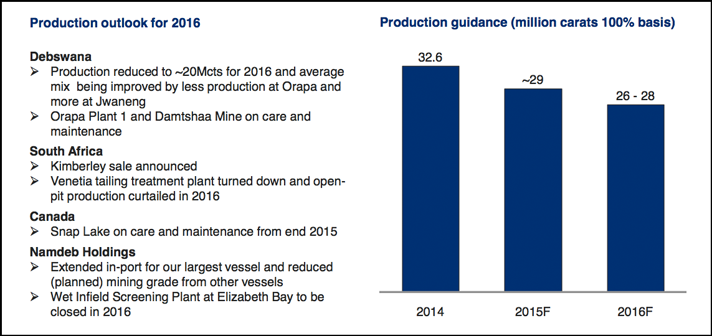

De Beers strategically cut its 2015 diamond production plan by 12% since the start of the year. Specifically, De Beers curtailed production at its more nimble Venetia tailings operation, sold its Kimberly tailings operation to Petra Diamonds (LSE: PDL), both in South Africa, put one of its Orapa processing plants on care-and-maintenance in Botswana, and put its 1M+ carat-annual-production Snap Lake mine in Canada on care-and-maintenance.

International mine, Mirny, Russia. Source ALROSA.

ALROSA has been building inventory rather than curtailing production, with current inventory at >20M carats, compared to the company’s normal inventory of 12-14M carats. While ALROSA has not cut production this year, two weeks ago the company said it would consider production cuts if ‘normalized diamond consumption’ is not realized in 2016.

With ALROSA and De Beers (via Anglo American), now publicly traded companies, longer-term market forces should take additional production offline if conditions weaken further, as relative price declines make production unprofitable.

Just this week, Anglo American (LSE: AAL), De Beers’ parent, vowed to suspend, sell, or close any assets that are not estimated to remain cash-flow positive over the term of a typical commodity cycle. Given De Beers’ company-wide average cost per carat estimate of $101 in 2016, it would take a further 19.2% decline in diamond prices for the company to reach its cost of production, according to my analysis. The economics are different for every mine, so the result would be incremental, and the shift in marginal cost of production would of course play a role, but theoretically rough could only fall another ~20%, before most of De Beers production would be halted. The equivalent figure for ALROSA is 28.7%, according to my analysis.

De Beers 2016 production plan. Source: De Beers' Dec. 8, 2015 investor day presentation.

In addition, Rio Tinto (LSE: RIO) cut its production plan at Argyle by 10% this year, the largest producing diamond mine in the world by carat volume, and Dominion Diamond (TSX: DDC) is holding back lower quality goods available for sale, according to my analysis based on inventory and sales figures.

According to 30-years of data from both ALROSA and De Beers, the industry historically reaches catharsis after 18-24 months of declining diamond prices and subsequent production response, which would indicate an end to the current downturn sometime around the middle of 2016.

Chow Tai Fook (HK: 1929), Greater China's largest diamond retailer, indicated they believe the current supply overhang is about 6 months from being cleared.

At the time of writing the author held a long position in Dominion Diamond Corp and Mountain Province Diamonds. Please read full disclosure below. The views expressed are strictly that of Paul Zimnisky, and are based solely on observations and opinions. Paul Zimnisky has made every effort to ensure the accuracy of information provided, however, accuracy cannot be guaranteed. Information in this article is strictly for informational purposes and should not be considered investment advice. Consult your investment professional before making any investment decisions.

Join the conversation daily at CEO Chat, the investment conference in your pocket.