Robert Friedland

Prior to the Ivanplats IPO in 2012, the Wall Street Journal and Bloomberg had both published articles speculating on an offering value of up to a billion dollars (the IPO was eventually completed as a $300-million offering). The company was founded by Robert Friedland, one of the best known mining developers, and had assembled three significant high-grade projects.

Plenty has changed since, the least of which being the company’s name - they retrieved the name Ivanhoe Mines as part of the sale of the Oyu Tolgoi property to Rio Tinto. Platinum and copper have since endured a precipitous downfall, both sliced in half in 3 years. What was a $4.75 IPO, is now trading at 53 cents per share. Like many things in the resource sector, the share price doesn’t tell the whole story.

Let’s look at what the company now has, starting with their cash position.

On December 8th Ivanhoe Mines received an initial payment from Zijin Mining - $206 million for 49.5% of Kamoa Holding Ltd (which held 95% ownership of the Ivanhoe Kamoa project). Over the next year and a half, Ivanhoe will receive payments of US$41.2 million every 3 and a half months, for a total value of US$412 million. Exclusive of current liabilities, those payments would put Ivanhoe’s current cash position at approximately US$530 million, or $716 million Canadian. Ivanhoe definitely has cash, for now (more on that later).

They have projects ...

Ivanhoe’s deal with Zijin Mining valued Kamoa at US$832 million - a 196% premium to Ivanhoe’s current US$281-million market cap. Zijin has also agreed on a best-efforts basis to secure non-recourse project financing for 65% of Kamoa. Partners like that are extremely rare in any market, let alone this one.

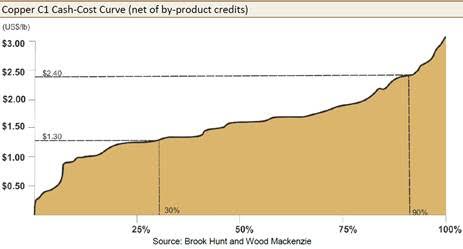

Should they succeed, Ivanhoe will be responsible for 17.5% of development capital - or an estimated US$245 million. Kamoa is 43 billion pounds of 2.67% copper (indicated), located in the Katanga province of the Democratic Republic of the Congo. The company’s stated cash costs of US$1.18 per pound of copper is in the bottom quartile of the cash cost curve.

Valuing the company’s Platreef project is difficult. Itochu Corp purchased a 10% stake in Platreef in 2012, the most recent 8% tranche for US$280 million, giving the project an implied valuation of US$3.5 billion. But 2012 was a lifetime ago.

Early last year Ivanhoe completed a pre-feasibility study for the first phase of Platreef to assess the project’s economics. Platreef ranks at the bottom of the cash-cost curve, at an estimated US$322 per ounce of 3PE+Au, net of by-products. Since the release of the pre-feasibility the price of platinum has dropped 37%, somewhat offset by the 35% decline in the South African rand.

Platreef’s internal rate of return of 13% isn’t staggering, but context is important: this is a deposit that could conceivably be mined into the 22nd century. It’s difficult to create an economic model for a mine that could endure many commodity cycles.

Of their $530 million, US$61 million is earmarked for the development of Platreef’s Shaft 1. They will need to arrange further project financing, no easy task given an estimated pre-production capital requirement of US$1.2 billion. Mining analyst Alex Terentiew from Raymond James expects “Platreef’s Japanese partners, who collectively own 10% of the project, to increase their ownership by another 10% during 2016, thereby providing financing for the project to continue until mid-2017, by [their] estimates.”

Finally, the Kipushi project. Unlike the other two projects, this is not a Friedland discovery. Ivanhoe’s 68% interest in the project was acquired for $150 million in 2011. Kipushi is a brownfield underground project also located in the DRC and previously mined between 1924 and 1993.

It’s likely the lowest priority of Ivanhoe’s projects, but there is significant potential: “Big Zinc” has some of the highest grades worldwide, Kipushi already has several expensive sunk shafts and zinc is one of the few commodities that, at the moment, has favorable investor interest. Even in a tough commodity environment, it’s quite conceivable that Kipushi will attract project financing.

They know how to spend money

Ivanhoe has a significant burn rate, spending over US$25 million a quarter. It’s a very expensive task to advance all three assets at once. It is clear, though, that the market currently expects a significant amount of their cash to be spent pre-development. The good news is that Zijin Mining will now be covering half the costs of Kamoa on a go-forward basis.

They have a world class financier with skin in the game

While most companies struggle to raise capital, Friedland has proven time and time again that he can finance Ivanhoe Mines - at the corporate andproject level - at a premium to market value. And with over 167 million shares, Friedland is invested.

At the Sprott Stansberry Natural Resource Symposium in the summer Friedland mentioned that Ivanhoe Mines was trading just above his 18-year average cost of 62 cents, as he stated “priced for Armageddon.”

Sitting at 53 cents now, there aren’t many situations where you can align yourself with management like you can with Ivanhoe. Importantly, while the rest of the market is running away from this space, this group has the foresight to do the opposite. For that reason alone, while cash is king, don’t rule out Ivanhoe acquiring another project.

On the commodity front, we are in dangerous territory at the moment. In a recent Metals and Mining report, Haywood Research noted that “approximately 30% of world copper production is uneconomic at current spot prices on an ‘all-in’ basis.” Using a cost curve from SNL Metals and Mining, the platinum industry is in even more dire straits.

Something has to give, and my guess is 2016 is the year that we finally see bankruptcies and production shut in’s on the supply side. The current commodities glut has caused many of the world’s miners to significantly slash capital expenditures. Pair that with declining grades and the market may rebalance sooner than currently anticipated. Frankly, if Ivanhoe’s two main projects - Kamoa and Platreef- aren’t economic long-term, then what projects are?

They have a significant amount of work to do

I can’t imagine waking up to the to-do list on Friedland’s fridge. Financing and developing three large projects in the midst of a commodities bust is a tall task. There’s likely no silver bullet to accomplish all that they need to, leaving the market with clear anxiety. The upside is that time is on their side. While all mining companies are struggling to stay afloat, Ivanhoe needs only to continue tackling milestones, and are funded to do so.

Moving forward, Kamoa Holdings is to divest another 15% to the Democratic Republic of Congo on commercial terms. That will leave Ivanhoe Mines and Zijin Mining with approximately 40% each, and the DRC 20%. The announcement of terms is likely to come soon, with agreed-upon development plans for Kamoa.

Furthermore, Ivanhoe should soon be out with a pre-feasibility study on the project, as well as an inaugural resource estimate for Kipushi. There’s also the matter of the escrowed shares. Every quarter - save for the first - since the IPO of the company there have been over 30 million shares released from escrow. This has been a significant overhang for the company. The final batch of shares will be released on January 23.

There will be a time again when Bloomberg and the Wall Street Journal return to the mining space along with the capital that follows it; that may not happen right away. Right now, it’s tough to ignore all of the value inside this company.

In the resource industry, there are no perfect investments. There’s environmental, social, geopolitical, and economic issues that spring up every day, that’s the nature of the business. All you can do is measure the risk that you take, balance the reward that could conceivably be reaped and handicap the likelihood of each situation happening.

At 53 cents, for a patient investor with a strong stomach, I think there are few companies that represent such an attractive risk/ reward.

Have an opinion on Ivanhoe? I’d love to hear it. Give me a call - (604) 697- 6178.

Ivanhoe Mines (IVN-T)

Price: $0.53

Market Cap: C$409 million

The above article was written by Riley Skinner, a registered Investment Adviser with Haywood Securities Inc., a Canadian-based independent, full‐service investment firm and member of the Canadian Investor Protection Fund. The article is for informational purposes only and is neither a solicitation for the purchase of securities nor an offer of securities. Readers of the article are expressly cautioned to seek the advice of a registered investment advisor and other professional advisors, as applicable, regarding the appropriateness of investing in any securities or any investment strategies, including those discussed above. The information contained in the reports have been compiled from sources Haywood believes are reliable; however, Haywood makes no guarantee, representation or warranty, expressed or implied, as to such information’s accuracy or completeness. The views expressed are those of the author and not necessarily Haywood Securities Inc. All opinions and estimates contained in the reports are based on assumptions the author believes to be reasonable as of the dates of the reports but are subject to change without notice. Either the author, Haywood Securities Inc. or its employees may from time to time hold or transact in the securities mentioned. Riley can be reached at 604-697-6178 or rskinner@haywood.com