Since topping out above US$4.50/lb in 2011, copper has fallen by more than 50% to a recent low of $1.94/lb. The 5-year copper bear market can be primarily blamed on soft Chinese demand and bloated Chinese copper inventories resulting from the 2009-2010 Chinese economic stimulus plan.

But there are some technical signs that the copper bear may have come to an end after 5 grueling years:

During the last couple of weeks, copper has broken out from the falling wedge that formed during 2015. The upside target from this chart pattern breakout is ~$3.

Meanwhile, Chinese copper imports have improved reaching the highest level of monthly imports in two years last month:

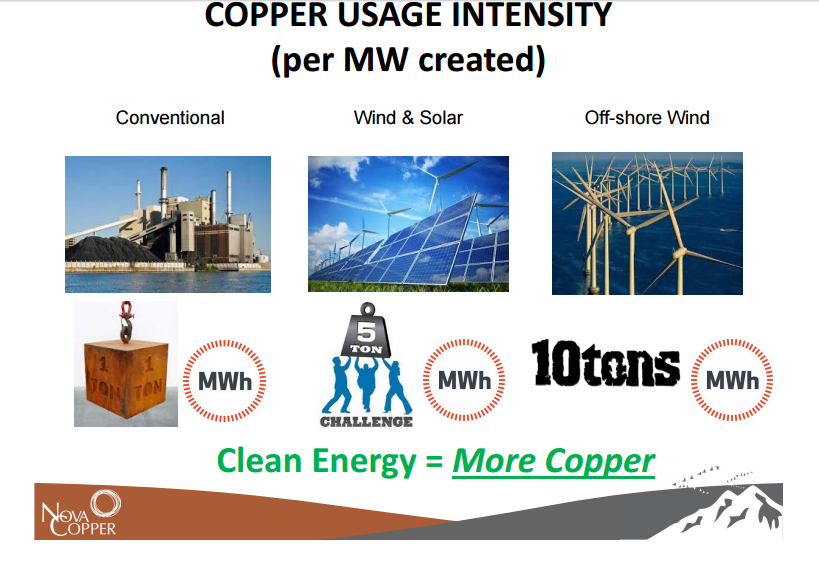

While copper faces a mixed picture in the near term the long-term copper story revolves around clean energy and the voracious growing global appetite for energy:

Copper, a key component of solar and wind, is a crucial component in the clean energy story:

Chinese consumers continue to purchase cars at a stunning rate and the government has rolled out a subsidy program incentivizing purchases of electric vehicles. Those sales have skyrocketed four-fold in the last year, and electric vehicles use 3X more copper (150 lbs) than a standard vehicle:

In order to meet the increasing demand over the next few decades, the world will need to develop the few large-scale economic copper resources in safe jurisdictions.

Enter NovaCopper and its Arctic and Bornite copper deposits in northern Alaska. Arctic boasts some impressive features including:

- 12-year mine life at 10,000 tonnes per day

- 95Kt (210M lbs) Annual Payable Cu Eq Production

- 125M lbs payable Copper per year

- 152M lbs payable Zinc per year

- 24M lbs payable Lead per year

- 29,000 oz payable Gold per year

- 2.5M oz payable Silver per year

- Cash costs of US$0.62/lb of payable copper net of by-product credits

- “All-in” cash costs of $US1.26/lb (Initial and sustaining capex, opex, TC/RCs, royalties…)

- Capital costs (Q2 2013): US$717.7 million startup, US$164.4 million sustaining

- Low capital intensity of $6,995/t (Industry Avg. +$14,000/t)

- Pre-Tax NPV8% of US$927.7 million using a $2.90 copper price assumption

- IRR of 22.8%

- Payback of 4.6 years using base case metals prices*

- Post-Tax NPV8% of US$537.2 million

- IRR of 17.9%

- Payback of 5.0 years using base case metal prices*

Arctic and Bornite, located 25 kilometres away from each other, host a combined 8 billion pounds of copper in the Indicated and Inferred categories. When byproduct credits are included, the resource estimate grows to 9.5 billion pounds of copper equivalent, Indicated and Inferred.

The sticking point for NovaCopper has been the construction of a 322-kilometre access road to the Dalton Highway, which would link the Ambler mining district to the deep-water, year-round ice-free port at Port Mackenzie. The company has signed a Memorandum of Understanding (MOU) with the Alaska Industrial Development & Export Authority (AIDEA). AIDEA has recently submitted the permit application (Consolidated Right-of-Way Application) to the Corp. of Engineers and other relevant State and Federal permitting agencies. The document is currently being reviewed for completeness. Once deemed “complete” the “Notice of Intent” will be issued which officially starts the EIS process (Environmental Impact Study) under NEPA (National Environmental Policy Act). Although a thorough and lengthy process, it is supported by the State of Alaska, NANA (Regional Alaska Native Corporation) and the two northern Alaska Boroughs governments – the Northwest Arctic Borough and the North Slope Borough. Although it will take time, with this support it is very likely to succeed.

The plan is to follow a toll-road-style agreement similar to what the State of Alaska has done with Teck’s Red Dog Mine. This would essentially equate to a low-cost loan for NovaCopper, to be repaid with production.

With “all-in” cash costs of US$1.26/lb -- which includes initial and sustaining capex, opex, TC/RCs, royalties etc. -- NovaCopper’s Arctic/Bornite copper projects are simply too compelling from an economic standpoint to not be brought into production. It’s simply a matter of getting the access road built and moving through the 2-3 year permitting process. The numbers are there, even at US$2/lb copper.

NovaCopper CEO Rick Van Nieuwenhuyse will be presenting at the Subscriber Investment Summit in Toronto on March 5, 2016. RSVP early to save your seat and follow NCQ on the TSX and NYSE.

Disclaimer:

This article includes certain “forward-looking information” and “forward-looking statements” (collectively “forward-looking statements”) within the meaning of applicable Canadian and United States securities legislation including the United States Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical fact, included herein, without limitation, statements relating to development of the Ambler mining district and advancement of the Arctic deposit, are forward-looking statements. Forward-looking statements are frequently, but not always, identified by words such as “expects”, “anticipates”, “believes”, “intends”, “estimates”, “potential”, “possible”, and similar expressions, or statements that events, conditions, or results “will”, “may”, “could”, or “should” occur or be achieved. These forward-looking statements may include statements regarding perceived merit of properties; exploration plans and budgets; mineral reserves and resource estimates; work programs; capital expenditures; timelines; strategic plans; market prices for precious and base metals; or other statements that are not statements of fact. Forward-looking statements involve various risks and uncertainties. There can be no assurance that such statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. Important factors that could cause actual results to differ materially from NovaCopper’s expectations include the uncertainties involving the need for additional financing to explore and develop properties and availability of financing in the debt and capital markets; uncertainties involved in the interpretation of drilling results and geological tests and the estimation of reserves and resources; the need for cooperation of government agencies and native groups in the development and operation of properties; the need to obtain permits and governmental approvals; risks of construction and mining projects such as accidents, equipment breakdowns, bad weather, non-compliance with environmental and permit requirements, unanticipated variation in geological structures, metal grades or recovery rates; unexpected cost increases, which could include significant increases in estimated capital and operating costs; fluctuations in metal prices and currency exchange rates; and other risks and uncertainties disclosed in NovaCopper’s Annual Report on Form 10-K for the year ended November 30, 2014 filed with Canadian securities regulatory authorities and with the SEC and in other NovaCopper reports and documents filed with applicable securities regulatory authorities from time to time. NovaCopper’s forward-looking statements reflect the beliefs, opinions and projections on the date the statements are made. NovaCopper assumes no obligation to update the forward-looking statements or beliefs, opinions, projections, or other factors, should they change, except as required by law.