Ten days ago before all the recent fun started we penned a piece entitled "2008 Redux?". The main point of this piece was to highlight the striking similarities between the current market and the lead up to the 2008 market meltdown. Most notably we just witnessed one of the worst months ever (September) for commodities and energy related stocks, meanwhile the S&P 500 barely budged from its all-time highs. A similar phenomenon took place in July/August 2008, just before the Lehman Brothers meltdown which took place in mid-September 2008.

Now that the S&P 500 has fallen nearly 9% from its all-time high posted less than one month ago, it's time to ask the question once again: Are we in for a 2008 redux?

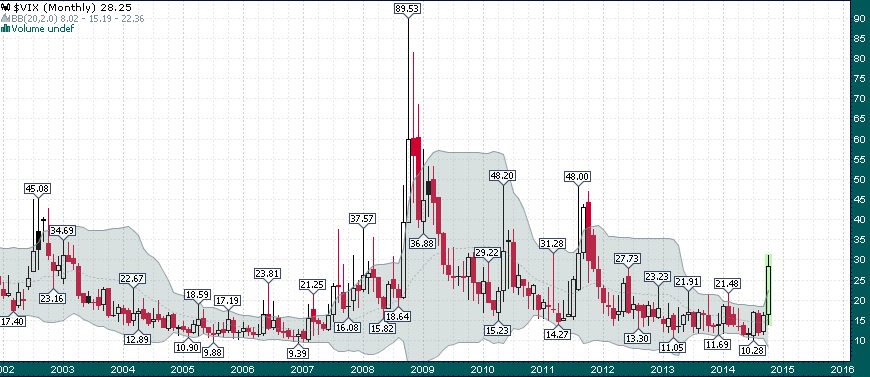

Judging by the structural damage that has been inflicted across markets and the incredible ramp up in volatility, we are certainly following the script quite closely. The VIX (S&P 500 Volatility Index) has lifted off in impressive fashion:

Click to enlarge

While the spike in volatility across markets has been nothing short of breathtaking, we've seen this movie before and with the exception of two notable examples (2008, summer 2011) markets have normalized and volatility has quickly subsided. A few things we will be looking for over the coming days:

- A VIX weekly close below 25 would indicate that Wednesday's huge spike was a short-term panic, whereas, a weekly close above 30 would offer a strong indication that elevated levels of volatility are here to stay for a while.

- Wednesday's low on the S&P 500 (1820) becomes an important 'line in the sand' - a breach of this level on a daily closing basis would be quite bearish.

- Wednesday morning's flight to Treasury securities (notes and bonds) was an '8-sigma event' (absolutely epic by any definition) - if Treasuries stay well bid it seems increasingly unlikely that the low is in for equities, equity bulls will want to see a sell-off in Treasuries.

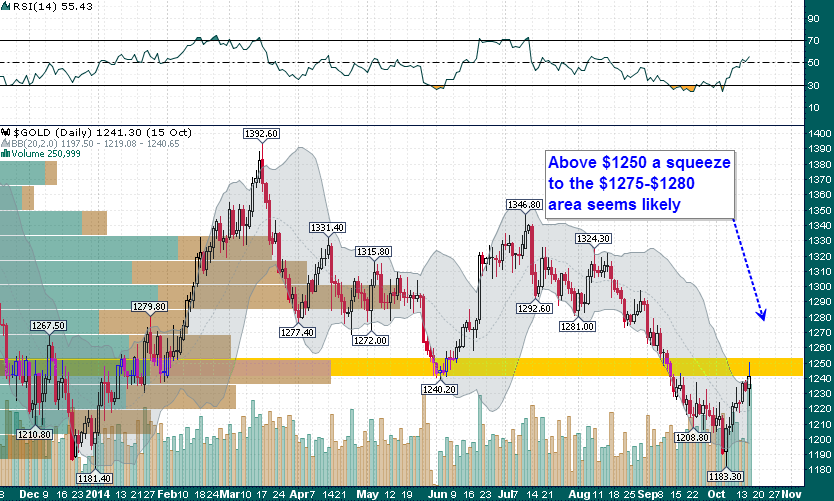

- Gold is facing some resistance near $1250, however, a break above this level is likely to trigger a substantial number of buy stops as we pointed out a couple weeks ago when sentiment was absolutely putrid on the yellow metal

In summary, this is a time to remain nimble and flexible and to not overcommit to any particular market view; those who kept dry powder and excercised patience were handsomely rewarded with ample opportunities in both 2008 and 2011.